Advertisement

CRM Software – Life insurance remains a critical component of financial planning, yet widespread myths about its cost, eligibility, and benefits continue to deter millions from securing adequate coverage. These misconceptions, often rooted in outdated information or incomplete understanding, obscure the reality that life insurance can be affordable, accessible, and beneficial across diverse life stages and health conditions. For example, studies by LIMRA reveal millennials frequently overestimate life insurance costs by up to 10 times, creating a significant barrier to early protection. Understanding the true nature of life insurance premiums, types of coverage, and the role policies play beyond death benefits is essential for making informed financial decisions.

The reality is that life insurance serves not only as a death benefit but also as a versatile financial tool that adapts to individual circumstances, including health impairments and family dynamics. From affordable term life options for young adults to cash-value policies offering living benefits, life insurance frameworks are more flexible and inclusive than commonly perceived. This article systematically debunks prevalent life insurance myths, presenting data-driven insights and expert analysis to clarify how policies operate, who benefits, and why personal coverage often complements or exceeds employer-provided plans.

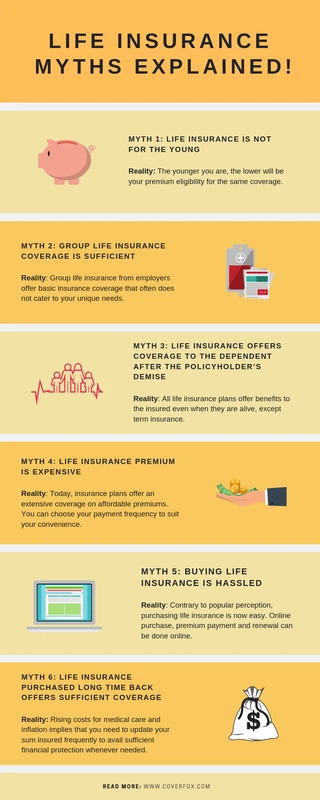

Myth #1: Life Insurance Is Too Expensive

Cost misconceptions are the most pervasive barrier preventing individuals, especially young adults, from obtaining life insurance. Research by the Life Insurance Market Research Association shows that millennials often believe life insurance premiums exceed their budgets by factors of five to twelve. However, term life insurance premiums for healthy males aged 25 to 35 average around $11 per month, making coverage affordable even on modest incomes.

Advertisement

This affordability is attributed to underwriting practices that price policies based on age, health status, and lifestyle factors. Term life insurance, which provides coverage for a specified period without cash value accumulation, typically offers the lowest premiums. For instance, a 30-year-old non-smoking female can secure a $500,000 term policy for less than $15 monthly, according to data from Pacific Life. Additionally, many insurers offer simplified issue and guaranteed issue policies requiring minimal underwriting, expanding access for those seeking quick coverage at competitive rates.

Despite these affordable options, the misconception persists partly because of confusion between term and permanent life insurance. Permanent policies, including whole and universal life, have higher premiums due to cash value components and lifelong coverage. Educating consumers on the suitability of term life insurance for initial protection can help dispel the myth that life insurance is prohibitively expensive.

Myth #2: Only Older or Main Earners Need Life Insurance

The belief that life insurance is only necessary for older adults or primary income earners ignores the financial risks faced by younger individuals and non-breadwinners. Research from Life Happens emphasizes that young adults often underestimate their financial responsibilities, including debts, future family needs, and the cost of replacing non-monetary contributions such as childcare, eldercare, or household management.

Non-breadwinners, including stay-at-home parents, students, or disabled individuals, contribute significant economic value that life insurance can protect. For example, the loss of a stay-at-home parent can result in substantial childcare expenses or lost household productivity. Insurance carriers like AAA Life and Western & Southern recognize this by offering policies tailored to non-traditional households and non-earners, reflecting an inclusive approach to risk protection.

Moreover, securing life insurance at a younger age provides premium advantages. Underwriting favors applicants with better health profiles and longer life expectancy, locking in lower rates that can remain fixed for decades. Early coverage also facilitates building cash value in permanent policies, enhancing future financial flexibility.

Myth #3: Life Insurance Benefits Are Only Paid After Death

Contrary to the common perception that life insurance only pays benefits upon death, many policies include living benefits accessible during the insured’s lifetime. Cash-value life insurance policies accumulate savings components that policyholders can borrow against or withdraw for emergencies, retirement supplementation, or major expenses.

Whole life and universal life insurance policies build cash value through a portion of premiums invested by the insurer. This cash value grows tax-deferred and can be accessed via policy loans or withdrawals, providing liquidity that can supplement income or cover medical costs. For example, Legal & General and Prudential offer living benefits riders that allow access to death benefits in cases of critical illness, chronic illness, or long-term care needs.

These features transform life insurance into a multifunctional financial asset, not merely a safety net after death. Awareness of living benefits broadens the appeal of permanent life insurance, especially for individuals seeking both protection and wealth accumulation.

Myth #4: Pre-existing Conditions Make Life Insurance Unaffordable or Unobtainable

Individuals with health impairments often assume life insurance is out of reach or prohibitively expensive. However, insurance carriers have developed underwriting models that evaluate risk more granularly, enabling many with pre-existing conditions to obtain coverage at reasonable rates.

Underwriting considers the type, severity, and treatment of health conditions alongside other risk factors. Some insurers, such as Ameriprise and Western & Southern, offer simplified issue policies requiring less medical information, while others provide graded benefit policies with partial payouts during initial years. Additionally, group insurance products through employers may offer coverage regardless of health, though typically with lower benefit limits.

For example, a diabetic applicant with controlled blood sugar levels may qualify for standard or slightly higher premiums, depending on the insurer’s risk assessment. This nuanced underwriting approach mitigates the myth that health impairments preclude life insurance access, encouraging individuals to consult with agents who can match them to suitable products.

Myth #5: Employer-Provided Life Insurance Is Sufficient

Many employees rely solely on employer-provided group life insurance, assuming it offers adequate protection. However, group coverage often provides limited benefits, typically one to two times annual salary, which may not cover long-term financial obligations.

Moreover, employer-based policies are tied to employment status. Job changes, layoffs, or retirement can result in loss of coverage or require conversion to individual policies at higher premiums. A 2023 LIMRA survey found that 60% of workers had insufficient life insurance coverage, largely because they underestimated personal needs beyond employer benefits.

Personal life insurance policies provide tailored coverage amounts, beneficiary designations, and policy types aligned with individual financial goals. Insurance agents and financial advisors recommend supplementing group coverage with personal policies to ensure comprehensive protection.

Myth #6: Buying Life Insurance Is Too Complicated

The perception of life insurance as a complex product deters many from initiating coverage. However, advancements in technology and streamlined underwriting have simplified the application process. Many insurers offer online quotes, instant approvals, and digital policy management tools.

Insurance agents and financial advisors play a crucial role in demystifying product options, explaining policy features, and helping clients navigate choices between term and permanent insurance. Tools such as needs calculators and comparison platforms facilitate informed decision-making.

For example, Ritter Insurance Marketing provides educational resources and agent support tailored to different life stages and financial goals. These services reduce complexity and empower consumers to select appropriate coverage confidently.

Adjusting Life Insurance as Life Changes

Life insurance needs evolve with major life events such as marriage, childbirth, home purchase, or career changes. Regular policy reviews ensure coverage aligns with current financial responsibilities and goals.

Insurance carriers encourage policyholders to update beneficiary designations and increase coverage as needed. For example, adding a dependent may necessitate increasing death benefits to cover future education or healthcare costs.

Some permanent policies offer flexibility to adjust premiums or death benefits. Term life insurance can also be converted to permanent coverage in many cases, accommodating changing needs without new underwriting.

Proactive policy management helps maintain adequate protection and maximizes the value of life insurance as a financial planning tool.

FAQ

Is life insurance affordable for young adults?

Yes, term life insurance is particularly affordable for healthy young adults. Premiums can be as low as $10–$15 per month for substantial coverage amounts, as underwriting favors younger, healthier applicants.

Can people with pre-existing medical conditions get life insurance?

Many can obtain life insurance, although premiums may vary based on health status. Simplified issue and graded benefit policies increase accessibility for individuals with certain health impairments.

Does life insurance only pay out after death?

No. Permanent life insurance policies build cash value that policyholders can access during their lifetime for emergencies or financial needs. Some policies also include living benefits for critical or chronic illnesses.

Why isn’t employer-provided life insurance enough?

Employer coverage often provides limited benefits and may end with employment changes. Personal life insurance ensures continuous, adequate protection tailored to individual financial obligations.

How can I simplify buying life insurance?

Using online tools, working with licensed insurance agents, and consulting financial advisors can streamline the process. Many insurers now offer digital applications and instant quotes to reduce complexity.

Life insurance myths such as “it’s too expensive” or “only for older people” persist despite evidence to the contrary. Recognizing life insurance’s affordability, diverse benefits, and adaptability to individual circumstances empowers consumers to secure appropriate protection. As financial landscapes evolve, integrating life insurance into a broader financial plan ensures resilience against uncertainties and supports long-term security.

For further expert insights, visit Pacific Life’s life insurance myths debunked and Western & Southern’s life insurance myth resources.

Advertisement