Advertisement

CRM Software – Insurance policies differ significantly in coverage, cost, and benefits depending on their type—life, health, auto, or home insurance. Consumers aiming to secure the best value must navigate a complex landscape of premium calculations, policy features, and provider reputations. Leveraging unbiased online comparison platforms alongside professional brokers enhances the ability to tailor insurance choices to personal needs, budget constraints, and regional variations, especially within the Canadian marketplace. Understanding the nuances of each policy type and the mechanisms behind premium pricing is crucial for making informed decisions.

Insurance premiums are influenced by individual risk profiles, coverage limits, and additional benefits, which vary widely among providers like Economical Insurance, RBC Insurance, and GreenShield. Comparison tools such as PolicyAdvisor, Rates.ca, and CompareHealth facilitate instant access to multiple quotes, enabling side-by-side evaluation of price and coverage. This detailed analysis explores how consumers can effectively compare insurance policies across categories, the role of brokers versus direct purchases, and practical strategies to optimize insurance choices through customization and bundling.

Types of Insurance Policies and Their Core Features

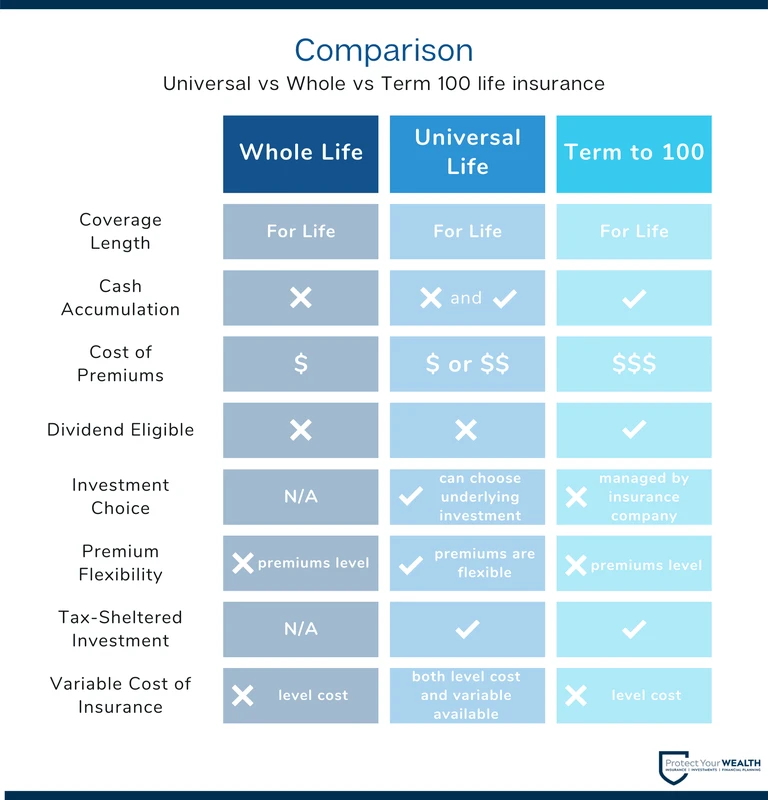

life insurance policies primarily fall into term life, whole life, permanent life, and guaranteed acceptance categories. term life insurance offers coverage for a specified period, typically 10-30 years, with premiums usually lower than permanent policies but without cash value accumulation. Whole life and permanent life insurance include an investment component that builds cash value over time, providing lifelong coverage but at higher premium costs. Guaranteed acceptance life insurance caters to individuals with health risks or older applicants, offering simplified underwriting but often at elevated premiums and lower coverage limits.

Advertisement

Health insurance plans encompass a range of benefits beyond basic medical coverage, including prescription drug plans, dental care, vision services, and emergency travel insurance. Providers like GreenShield specialize in supplemental health insurance that fills gaps left by public healthcare, offering customizable plans tailored to individual needs. Coverage specifics—such as annual maximums for dental or formularies for medications—vary by insurer, necessitating careful comparison of plan features.

Auto insurance policies cover liability, collision, comprehensive damage, and offer various discounts such as multi-vehicle or safe driver incentives. Liability coverage protects against bodily injury and property damage claims, while collision and comprehensive cover repairs to the insured vehicle. Providers like Economical Insurance and RBC Insurance offer regional variations in rates, reflecting provincial regulations and risk factors like urban density or theft rates.

Home insurance addresses property damage, liability protection, and specialized coverage for risks such as flooding or high-value personal property. Tenant and condo insurance provide tailored protection for renters and condo owners, often covering personal belongings, liability, and additional living expenses. Understanding the distinctions between these policies is vital, as coverage limits and exclusions differ markedly between homeowner, tenant, and condo insurance.

Effective Strategies for Comparing Insurance Policies

Online comparison platforms have transformed insurance shopping by aggregating quotes from multiple providers, enabling consumers to review premiums, coverage limits, and policy features simultaneously. CompareHealth and Rates.ca offer no-commission, unbiased tools that generate personalized quotes based on detailed user inputs such as age, health status, location, and coverage preferences. These platforms often incorporate filters for plan benefits, provider ratings, and payment flexibility, aiding in granular comparisons.

insurance brokers provide expert guidance by assessing client circumstances and recommending policies from a curated network of insurers. While brokers can offer tailored advice and assist with claims, they may have access to a narrower selection of providers or receive commissions that influence recommendations. Conversely, purchasing directly from insurance companies might limit options but can offer streamlined processes and potential discounts for bundling policies within the same provider.

Key comparison factors include premium costs, coverage limits, policy exclusions, and available discounts. For example, bundling auto and home insurance typically yields premium reductions, while add-ons such as roadside assistance or enhanced dental coverage increase costs but may be worthwhile depending on individual risk assessments. Personalized quotes based on comprehensive data inputs are essential, as generic estimates can misrepresent actual premium obligations.

How Premiums Are Calculated and Factors Affecting Renewal Rates

insurance premiums reflect the insurer’s assessment of risk, influenced by variables including age, health conditions, driving history, property location, and claims history. Life insurance underwriting evaluates mortality risk, with higher premiums for smokers or individuals with pre-existing conditions. Health insurance premiums depend on coverage scope and deductible levels, with age and medical history as primary determinants.

Renewal premiums can increase due to changes in risk profiles, inflation, or claims experience. For auto insurance, a history of accidents or traffic violations often results in higher renewal rates. Home insurance renewal premiums may rise after property damage claims or due to market-wide adjustments for increased rebuilding costs. Bundling policies often stabilizes premiums by providing insurers with a broader view of risk across multiple coverage areas.

Understanding these dynamics enables consumers to anticipate premium fluctuations and negotiate better rates during renewal. Regularly comparing renewal quotes against market offerings is advisable to ensure ongoing value.

Practical Tips for Selecting the Optimal Insurance Policy

Evaluating personal risk factors and coverage needs is the foundation of effective insurance selection. For life insurance, consumers should consider financial responsibilities such as mortgage debt, dependents, and long-term savings goals. Health insurance purchasers benefit from analyzing anticipated medical expenses, prescriptions, and preferred providers. Auto insurance selection should account for driving frequency, vehicle value, and liability exposure, while home insurance decisions depend on property type, location-specific risks, and possessions’ value.

Reading policy fine print is critical to uncover exclusions, waiting periods, and claim procedures that impact actual coverage. For example, some health plans exclude pre-existing conditions or limit dental reimbursement. Long-term benefits, such as cash value accumulation in permanent life insurance or no-claim bonuses in auto insurance, must be weighed against upfront premium costs.

Professional advice from licensed brokers or independent advisors can clarify complex policy details and provide access to exclusive discounts or underwriting exceptions. Consumers should also periodically review insurance portfolios to adjust coverage as life circumstances evolve.

Case Studies: Comparing Insurance Quotes Across Providers

A comparison of term life insurance quotes between PolicyAdvisor and RBC Insurance reveals notable differences in premiums and underwriting criteria. PolicyAdvisor’s online platform provides instant quotes from over 50 providers, allowing users to compare term lengths and premium rates side by side. RBC Insurance, as a direct provider, offers fixed term options with bundled health and life benefits but with less price variability. Users leveraging PolicyAdvisor’s tool reported premium savings averaging 15-20% compared to direct applications.

In health insurance, GreenShield’s plans emphasize comprehensive prescription drug coverage and dental benefits, while CompareHealth aggregates plans with varying deductibles and vision care options. Consumers often find GreenShield suitable for chronic medication management, whereas CompareHealth’s broader marketplace facilitates cost-effective selection for general health needs.

For auto and home insurance, Rates.ca and Economical Insurance platforms demonstrate regional rate disparities driven by provincial regulations and risk assessments. Rates.ca’s comparison engine highlights multi-policy discounts, while Economical’s direct offerings include customizable add-ons such as identity theft protection and eco-friendly vehicle incentives. Comparing these providers enables consumers to tailor coverage and optimize premiums effectively.

Insurance Type |

Key Coverage |

Typical Premium Factors |

Comparison Platform Examples |

Notable Benefits |

|---|---|---|---|---|

Life Insurance |

Term length, cash value, death benefit |

Age, health, smoker status |

PolicyAdvisor, RBC Insurance |

Guaranteed acceptance options, investment component |

Health Insurance |

Prescription, dental, vision, emergency travel |

Age, coverage scope, medical history |

GreenShield, CompareHealth |

Supplemental coverage, flexible deductibles |

Auto Insurance |

Liability, collision, discounts |

Driving record, vehicle type, location |

Rates.ca, Economical Insurance |

Bundling discounts, customizable add-ons |

Home Insurance |

Property damage, liability, specialized coverage |

Home value, location, claims history |

Rates.ca, Economical Insurance |

Flood and high-value item coverage, multi-policy discounts |

FAQ

What is the best way to compare life insurance policies?

The most effective method is using unbiased online comparison tools like PolicyAdvisor that provide personalized quotes from multiple insurers, combined with evaluating policy details such as term length, coverage limits, and cash value features to align with your financial goals.

Are online insurance comparison tools reliable?

Yes, platforms like Rates.ca and CompareHealth offer reliable, up-to-date quotes by aggregating data directly from insurers and applying personalized inputs. However, verifying coverage specifics and exclusions in the policy documents is essential.

How do I know if I am getting the cheapest car insurance rate?

Obtaining multiple quotes through comparison platforms and considering your driving history, vehicle type, and location will give a clear view of competitive rates. Also, inquire about available discounts and bundling options to reduce premiums.

Can I customize my home insurance coverage?

Most home insurance policies allow customization through add-ons such as flood protection, identity theft coverage, or enhanced personal property limits. Discuss these options with your provider or broker to tailor your plan.

Is it better to buy insurance directly or through a broker?

Both have advantages: brokers offer personalized advice and access to multiple insurers, while direct purchases may provide streamlined service and discounts. Choosing depends on your comfort with evaluating policies and the complexity of your insurance needs.

Insurance policy comparison in 2026 demands an informed approach that balances cost, coverage, and provider reliability. Utilizing advanced online tools alongside expert broker consultations empowers consumers to optimize insurance portfolios effectively. Monitoring renewal trends and revisiting coverage periodically ensures sustained value and protection tailored to evolving personal circumstances.

For more detailed insurance policy comparisons and personalized quotes, visit PolicyAdvisor’s life insurance quotes and Rates.ca insurance comparison platform.

Advertisement