Advertisement

CRM Software – The insurance claims process is a structured series of steps that a policyholder follows to receive compensation from an insurance company after experiencing a loss covered under their policy. This process begins immediately after reporting the loss to the insurer or broker and involves collecting evidence, undergoing a detailed claim investigation, reviewing the policy’s coverage terms, and ultimately receiving payment, which often includes an initial advance followed by final settlement payments. The role of claims adjusters, insurance brokers, and replacement vendors is pivotal, as they facilitate damage assessment, negotiate coverage, and ensure proper reimbursement. Understanding each phase of this process, including the documentation required and the typical timelines, is crucial for policyholders to navigate claims efficiently and avoid common pitfalls such as delayed filing or inadequate documentation.

Each insurance claim is fundamentally governed by the terms outlined in the insurance policy, which dictates coverage limits, exclusions, and claim procedures. For example, auto insurance claims require adherence to Fault Determination Rules which assign liability and influence settlement amounts. Home and business insurance claims follow similar yet distinct protocols depending on the nature of the loss and policy conditions. The initial report of loss must be timely, as delays can lead to claim denial. Claims adjusters conduct onsite inspections to verify damage, while brokers provide advocacy and guidance throughout the process. Payments are typically disbursed as advances to cover immediate costs, with final settlements contingent upon proof of replacement or repair expenditures. This layered approach ensures transparency and accountability for both policyholders and insurers.

Understanding the Insurance Claims Process

An insurance claim is a formal request by a policyholder to an insurance company for financial reimbursement or coverage for losses sustained under the terms of an insurance policy. Filing a claim initiates a complex process designed to verify the loss, assess responsibility, and calculate compensation based on the policy’s coverage. The primary purpose of filing an insurance claim is to transfer the financial burden of an unexpected event—such as a car accident, property damage, or business interruption—from the policyholder to the insurer.

Advertisement

The claims process serves multiple functions: it prevents fraud through thorough investigation, ensures compliance with legal and contractual obligations, and facilitates timely payment to policyholders. Each claim is unique, influenced by the type of insurance—be it auto, home, or business—and the specific circumstances surrounding the loss. Understanding the definition and purpose of an insurance claim provides the foundation for navigating the subsequent steps effectively.

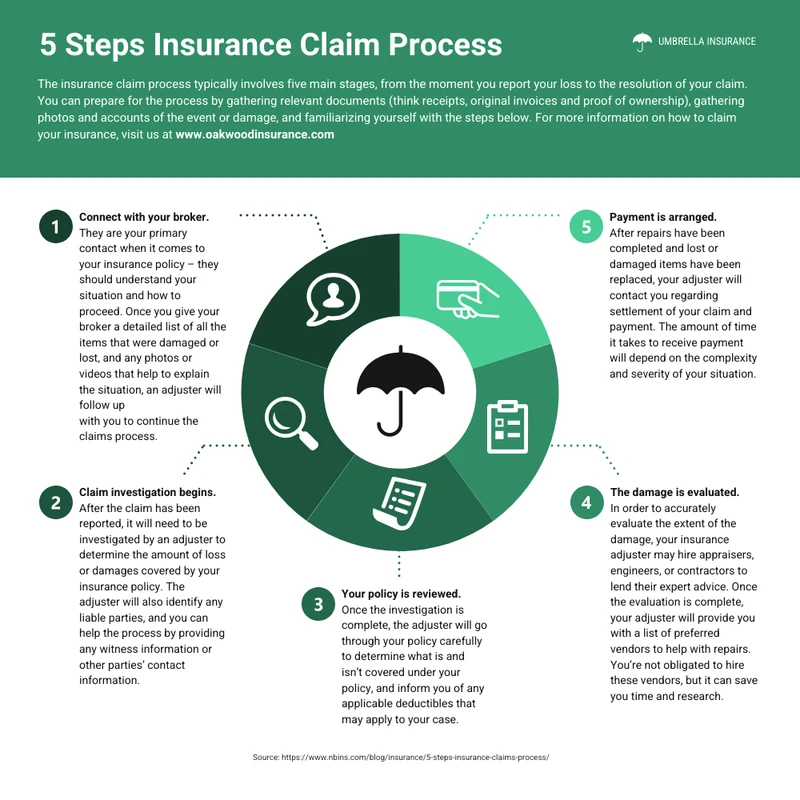

Step-by-Step Breakdown of the Insurance Claims Process

1. Reporting the Loss or Incident

The first and most critical step in the insurance claims process is promptly reporting the loss to the insurer or insurance broker. Immediate reporting safeguards the policyholder’s eligibility and triggers the insurer’s obligation to investigate and process the claim. Typically, policyholders can report losses via phone hotlines, insurer websites, or mobile apps designed for claims intake. For example, many insurers now offer 24/7 claims hotlines to expedite initial reporting.

During this step, safety is paramount. In cases such as auto accidents or home fires, policyholders are advised to secure the scene, seek medical attention if needed, and document initial damage through photographs or videos. This documentation serves as primary evidence during claim evaluation. Reporting the loss also involves completing initial forms or statements detailing the incident’s circumstances.

2. Documentation and Evidence Collection

Supporting documentation is essential for validating the claim and demonstrating the extent of the loss. Required documents typically include receipts for damaged or lost items, photographs or videos showing the damage, police reports in cases of theft or accidents, and medical records if injuries are involved. Policyholders should retain damaged items until the adjuster has inspected them, as premature disposal can complicate claim validation.

The Proof of Loss form is a critical document that policyholders must submit, outlining the details of the claim and the amount being claimed. This form often requires notarization and must be submitted within specific deadlines mandated by the insurer or state regulations. Additionally, receipts for cleanup services or temporary repairs can strengthen the claim by evidencing the necessity and cost of immediate mitigation efforts.

3. Claim Investigation and Adjustment

Once a claim is reported and initial documentation submitted, the insurance company assigns a claims adjuster to investigate. The adjuster’s role is to inspect the damage firsthand, assess the validity of the claim, and estimate repair or replacement costs. This process may involve onsite visits, interviews with the policyholder and witnesses, and consultation with contractors or replacement vendors.

Claims adjusters utilize specialized tools and software for damage assessment, such as auto estimating systems or home restoration cost databases, to ensure accurate evaluations. Adjusters must also verify that the loss falls within the policy’s coverage scope and complies with any applicable exclusions or limits. Their findings form the basis for the insurer’s settlement offer.

4. Review of Policy Coverage and Eligibility

After the adjuster completes their assessment, the insurer reviews the policy terms to determine eligibility and coverage limits. This review includes analyzing deductibles, sub-limits, and any exclusions that may apply. For auto claims, Fault Determination Rules are applied to assign liability and influence the settlement amount. These rules vary by jurisdiction but generally categorize fault percentages to guide premium adjustments and payment responsibilities.

Understanding coverage nuances is essential for policyholders, as certain damages may not be covered, or compensation may be capped. For instance, some home insurance policies exclude damage caused by floods or earthquakes unless additional riders are purchased. Clear communication with insurance brokers or representatives can clarify coverage details and manage expectations.

5. Compensation and Payment Procedures

Insurance payments typically occur in stages. Initially, insurers may issue an advance payment to cover urgent expenses such as temporary housing or vehicle repairs. This advance is not the final settlement but provides immediate financial relief. The final compensation is contingent upon submission of proof of replacement purchases, repair invoices, or receipts.

Payment timelines vary but generally follow regulatory guidelines requiring insurers to process claims within 30 to 45 days of receipt of all necessary documentation. Insurers may also issue multiple payments for complex claims involving phased repairs or staged business recovery. Policyholders should track payments and maintain clear records to reconcile disbursements with incurred expenses.

6. Working with Insurance Professionals

Insurance brokers and claims representatives play vital roles in facilitating a smooth claims process. Brokers serve as advocates, helping policyholders understand policy language, gather documentation, and communicate effectively with the insurer. Claims representatives manage claim processing logistics and can provide updates on claim status.

Preferred vendors and contractors often collaborate with insurers to expedite repairs or replacements. Working with these approved service providers can streamline the process, as insurers may have pre-negotiated rates or direct billing arrangements. However, policyholders retain the right to choose their own vendors, though this may impact payment timelines.

7. Follow-up, Disputes, and Reopening Claims

Claims may require reopening if additional damages are discovered after initial settlement or if repairs uncover further issues. Policyholders must notify the insurer promptly and provide new evidence to justify reopening the claim. Disputes can arise over coverage interpretation, settlement amounts, or fault determination.

In such cases, formal appeals processes or mediation may be necessary. Some jurisdictions mandate independent appraisal or arbitration to resolve claim disputes. Maintaining comprehensive documentation and clear communication is crucial for successful dispute resolution.

Variations in Claims by Insurance Type

Auto insurance claims often involve detailed fault determination and may include medical claims, property damage, and liability components. For example, the Fault Determination Rules guide insurers in assigning responsibility and influence premium adjustments. Auto claims require police reports, repair estimates, and sometimes medical documentation.

Home insurance claims focus on physical property damage and personal property loss. Common claims include fire, theft, water damage, and natural disasters. Homeowners must navigate policy-specific exclusions, such as those for flood or earthquake damage, unless additional coverage was purchased. Documentation includes repair estimates, photos, and receipts for temporary housing if displacement occurs.

Business insurance claims encompass a broader range of losses, including property damage, business interruption, liability claims, and employee-related claims. The complexity of business claims often necessitates detailed financial records, loss of income documentation, and coordination with multiple stakeholders.

Legal and Regulatory Considerations

Timely filing of insurance claims is mandated by state and provincial regulations, with deadlines varying typically between 30 and 90 days from the loss event. Failure to comply can result in claim denial. Additionally, fault determination rules, particularly in auto insurance, are codified by government agencies to ensure fair liability assignments.

Claims impact a policyholder’s insurance record and may influence future premiums. For instance, at-fault auto claims generally lead to premium increases, while no-fault claims may not. Understanding these legal frameworks helps policyholders anticipate consequences and plan accordingly.

Tips for a Smooth Claims Experience

Preparation before a loss occurs significantly improves claim outcomes. Policyholders should maintain organized records of their insurance policies, inventory of valuable items, and contact information for their insurer and broker. Keeping digital copies of receipts and photographs of possessions aids in faster claims processing.

Effective communication with insurers involves promptly responding to requests, keeping detailed notes of conversations, and using claims tracking tools or mobile apps offered by insurers for real-time updates. Engaging with brokers early in the process can provide guidance tailored to specific policy conditions.

Using claims tracking tools enhances transparency, allowing policyholders to monitor progress and document correspondence. Many insurers now offer apps that notify users of claim milestones, payment status, and adjuster visits, reducing uncertainty and improving satisfaction.

Claim Type |

Key Documentation |

Unique Considerations |

Typical Timeline |

Common Payment Structure |

|---|---|---|---|---|

Auto Insurance |

Police report, repair estimates, medical records, photos |

Fault determination rules, liability assignment, medical claims |

30-45 days |

Advance payment for repairs, final settlement after proof |

Home Insurance |

Photos, repair estimates, receipts for temporary housing |

Exclusions for flood/earthquake, displacement coverage |

30-60 days |

Initial advance for emergency repairs, final payment post-invoice |

Business Insurance |

Financial loss documents, property damage reports, income statements |

Complex claims, multi-stakeholder coordination, business interruption |

45-90 days |

Staged payments based on recovery phases |

This table summarizes documentation needs, unique aspects, timelines, and payment structures for different insurance claim types, providing a quick reference for policyholders.

FAQ

What documents are essential when filing an insurance claim?

Essential documents include a completed Proof of Loss form, photographs or videos of the damage, receipts or invoices for repairs or replacement, police or incident reports if applicable, and communication records with the insurer. Retaining damaged items until inspected is also important.

How long does the insurance claims process typically take?

The timeline varies by claim type and complexity but generally ranges from 30 to 90 days after submission of all required documentation. Auto claims often settle within 30-45 days, while business claims may take longer due to financial assessments.

Can I choose my own contractors or repair vendors for a claim?

Policyholders can select their own contractors, but insurers often recommend preferred vendors to expedite repairs and manage costs. Using non-preferred vendors may delay payment or require additional documentation.

What happens if my insurance claim is denied?

If denied, policyholders have the right to request a detailed explanation and may appeal the decision through insurer dispute resolution processes, mediation, or legal action if necessary. Maintaining comprehensive records supports appeals.

How do fault determination rules affect auto insurance claims?

Fault determination rules assign responsibility for accidents, influencing which insurer pays and how premiums may be adjusted. These rules vary by jurisdiction but provide standardized guidelines for liability and compensation.

Understanding and navigating the insurance claims process requires attention to detail, timely action, and effective collaboration with insurance professionals. Policyholders who document thoroughly, communicate clearly, and utilize available tools can significantly improve their claims experience and ensure fair compensation.

For further detailed guidance on the steps involved in insurance claims, visit the Northbridge Insurance claims process overview and the Insurance Information Institute’s payment process article.

Advertisement