Advertisement

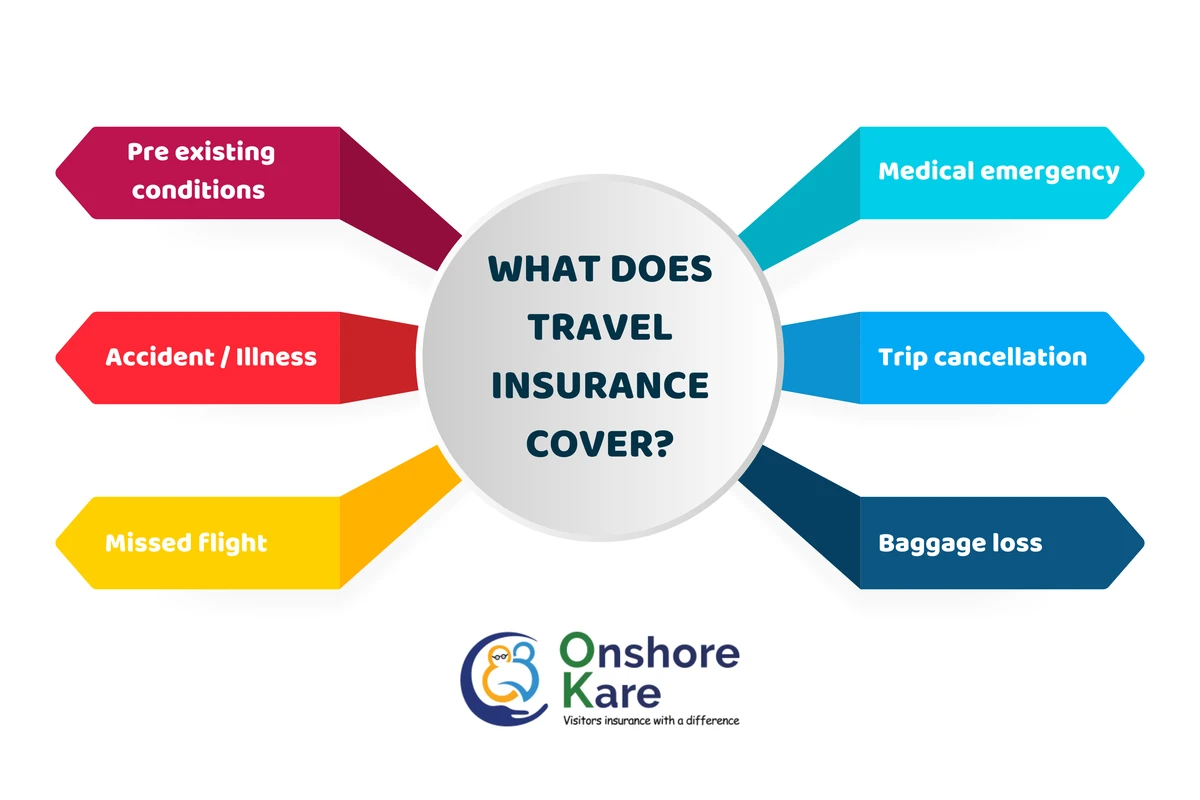

CRM Software – Travel insurance is designed to mitigate financial risks associated with unforeseen events during travel, including medical emergencies, trip cancellations, baggage loss, and delays. It offers protection beyond provincial health plans, particularly for Canadians traveling internationally, where healthcare costs can be prohibitively expensive and sometimes not covered by domestic insurance. Coverage typically includes emergency medical expenses with limits ranging from CAD 3 million to CAD 5 million, reimbursement for non-refundable trip costs due to covered reasons, compensation for lost or damaged baggage, and allowances for travel delays such as meals or accommodations. However, coverage is contingent on policy terms, with deductibles, exclusions, and travel advisories significantly affecting claim eligibility.

Emergency medical coverage forms the backbone of most travel insurance plans. This segment includes hospital stays, physician fees, ambulance transport, and occasionally prescription medications incurred abroad. Given that provincial health plans often provide limited or no coverage outside Canada, travel insurance fills this critical gap. For example, Allianz Global Assistance offers plans with emergency medical coverage up to CAD 5 million, which can prevent catastrophic out-of-pocket expenses. It’s essential to understand that coverage limits vary by provider, and deductibles—typically ranging from CAD 0 to CAD 250—impact out-of-pocket costs. Additionally, many insurers exclude coverage for pre-existing medical conditions unless disclosed and approved, underscoring the importance of transparent health declarations.

Trip cancellation and interruption insurance reimburses travelers for non-refundable expenses when a trip is canceled or cut short for covered reasons such as illness, family emergencies, or severe weather events. This coverage also extends to unforeseen events like jury duty or travel advisories issued by government bodies such as the Canadian government’s official travel advisories. For instance, if a traveler must cancel a trip due to a sudden hospitalization, the insurance provider reimburses prepaid costs including flights, hotels, and tours, subject to policy limits. Multi-trip plans typically cover multiple trips within a 12-month period, offering cost efficiencies for frequent travelers, while single-trip plans are purchased per journey. Policy limits for cancellation coverage often reflect the total trip cost, emphasizing the need to insure the full non-refundable amount.

Advertisement

Baggage protection policies cover loss, theft, or damage to luggage and personal belongings during travel. Coverage amounts vary widely but typically range between CAD 1,000 and CAD 3,000 per person. Some insurers like Travel Guard include provisions for delayed baggage, providing reimbursement for essential items purchased while waiting for delayed luggage. It is important to note that some high-value items such as electronics or jewelry may have sub-limits or require additional endorsements. Travelers should maintain itemized lists and receipts to facilitate claims. According to industry reports, baggage loss claims represent approximately 15% of all travel insurance claims, demonstrating the prevalence and importance of this coverage.

Flight delay and missed connection coverage compensates for additional costs incurred due to delays beyond a specified threshold, commonly three to six hours. This includes meal expenses, overnight accommodations, and rebooking fees. However, some policies exclude delays caused by strikes or mechanical failures, which are common reasons for delays. Hence, travelers must carefully review the terms specifying covered delay reasons. For example, Travelex offers coverage for delays exceeding six hours, reimbursing up to CAD 500 per insured person for meals and accommodations, which can mitigate stress and out-of-pocket expenses during disruptions.

Understanding deductibles and coverage limits is crucial for evaluating travel insurance policies. Deductibles represent the amount a traveler must pay before insurance benefits apply, typically ranging from CAD 0 to CAD 250 depending on the plan. Coverage limits define the maximum payout for specific coverage types, such as emergency medical or baggage protection. Emergency medical limits often range from CAD 3 million to CAD 5 million, reflecting the high costs of healthcare abroad. Multi-trip plans generally impose per-trip day limits (e.g., 30 or 60 days per trip), which can affect travelers undertaking extended journeys. Family plans offer consolidated coverage for multiple travelers, often with cost savings compared to individual policies, and can include children under a certain age at no additional charge.

Government-issued travel advisories significantly influence travel insurance validity. Insurance providers often exclude coverage for destinations under official warnings due to conflict, epidemics, or natural disasters. For example, traveling to countries flagged by the Canadian government’s travel advisories as “Avoid Non-Essential Travel” may void coverage for trip cancellation or emergency medical claims. Travelers should consult the official Canadian travel advisory website prior to purchasing insurance and before departure to ensure destination eligibility. Some insurers provide coverage extensions if advisories are issued after policy purchase, but these are exceptions rather than the rule.

Emergency medical evacuation and repatriation represent critical components of travel insurance, covering transportation to the nearest adequate medical facility or back to the home country when local treatment is unavailable or insufficient. Evacuation costs can exceed CAD 50,000, making this coverage indispensable. Typical scenarios include evacuation by air ambulance following a serious accident or illness. Without insurance, travelers face potentially devastating financial liabilities. Providers like Allianz and Travel Guard offer evacuation coverage included in their medical plans or as add-ons, underscoring the importance of verifying this feature. Medical repatriation also covers returning remains in the event of traveler death abroad, a service often overlooked but emotionally and financially significant.

Common exclusions in travel insurance policies encompass pre-existing medical conditions, high-risk activities (e.g., extreme sports), travel to restricted or high-risk areas, and failure to comply with policy terms such as timely notification of claims. Pre-existing condition clauses vary, with some insurers requiring stable health periods before coverage applies. Adventure travel coverage is often excluded unless an add-on is purchased. For instance, skiing or scuba diving may require special endorsements. Understanding these exclusions is essential to avoid denied claims and unexpected costs. Policy terms frequently specify the requirement to seek medical care promptly and to retain documentation for claims processing.

Travel insurance interacts with other coverage sources such as provincial health plans, employer insurance, and credit card benefits. Provincial health plans provide limited or no coverage outside Canada, making travel insurance vital for international trips. Some employer plans may offer supplemental travel coverage, but these are typically insufficient for comprehensive emergency medical needs. Many credit cards provide travel insurance benefits when the trip is purchased using the card; however, coverage limits tend to be lower and subject to restrictive conditions, such as covering only a portion of emergency medical costs or excluding pre-existing conditions. Travelers should assess the adequacy of these overlapping coverages and consider purchasing standalone travel insurance to fill gaps.

Selecting the right travel insurance plan requires evaluating destination risk, trip duration, traveler age and health status, and the nature of planned activities. For example, seniors may require plans with higher medical limits and pre-existing condition coverage. Frequent travelers benefit from multi-trip plans with per-trip limits suited to their itinerary patterns. Adventure travelers should seek policies including or allowing add-ons for hazardous activities. Questions to ask insurers include: What are the maximum medical coverage limits? Are pre-existing conditions covered? What exclusions apply? Is emergency evacuation included? What are the policy deductibles? Obtaining clear answers ensures the selected policy aligns with travel needs and risk tolerance.

Filing claims effectively involves prompt notification to the insurer, thorough documentation including medical reports, receipts, and police reports where applicable, and adherence to deadlines specified in the policy. Most providers offer 24/7 emergency assistance services to guide travelers during crises, including help with hospital admissions, locating medical providers, and arranging evacuations. Utilizing these services can streamline claims and ensure timely assistance. Familiarizing oneself with the insurer’s claims process before departure reduces stress and expedites reimbursement.

Coverage Type |

Typical Coverage Limits (CAD) |

Common Deductibles (CAD) |

Coverage Notes |

|---|---|---|---|

Emergency Medical |

3,000,000 – 5,000,000 |

0 – 250 |

Covers hospital stays, ambulance, doctor visits, prescription drugs (varies) |

Trip Cancellation/Interruption |

Up to total non-refundable trip cost |

0 – 100 |

Reimburses prepaid expenses for covered reasons |

Baggage Loss/Delay |

1,000 – 3,000 |

0 – 100 |

Includes delayed baggage essentials reimbursement |

Flight Delay |

Up to 500 |

0 |

Meals, accommodation after delays exceeding threshold hours |

Emergency Evacuation |

Included in medical limits or separate |

Varies |

Air ambulance and repatriation costs |

This table summarizes typical coverage limits and deductibles found in Canadian travel insurance policies, illustrating the financial protection scope for travelers.

FAQ

What does travel insurance typically cover?

travel insurance generally covers emergency medical expenses, trip cancellations or interruptions for covered reasons, lost or delayed baggage, and travel delays. Coverage depends on policy limits, deductibles, and exclusions, and may be voided if traveling to destinations under official government travel advisories.

How do government travel advisories affect travel insurance?

Government-issued travel advisories can void insurance coverage for trips to high-risk destinations. Insurers typically exclude claims related to travel in countries flagged as unsafe or under “Avoid Non-Essential Travel” warnings. Checking advisories before purchase and departure is crucial.

Are pre-existing medical conditions covered by travel insurance?

Coverage for pre-existing conditions depends on the insurer and policy. Many plans exclude these conditions unless disclosed and approved, or unless the condition is stable for a specified period before travel. It is vital to review policy terms carefully.

Can credit card travel insurance replace standalone travel insurance?

Credit card travel insurance often provides limited benefits with lower coverage limits and exclusions, such as no coverage for pre-existing conditions. It may not adequately cover emergency medical costs abroad, so standalone travel insurance is recommended for comprehensive protection.

What should I do if I need to file a travel insurance claim?

Notify your insurer promptly, keep all relevant documentation (medical reports, receipts, police reports), and follow the insurer’s claims process. Many providers offer 24/7 emergency assistance to support travelers during emergencies.

Travel insurance remains an essential safeguard for travelers, especially Canadians venturing abroad where provincial health benefits fall short. Understanding the nuances of coverage types, policy conditions, and exclusions enables informed decisions that protect both finances and well-being. Future travel insurance offerings may increasingly integrate AI-driven risk assessments and dynamic pricing linked to real-time travel advisories, enhancing personalized coverage and claims processing efficiency.

For further detailed guidance on travel insurance coverage and exclusions, consult resources like Belair Direct’s travel insurance overview and the Ontario Long Term Care Health Insurance guide.

Advertisement