Advertisement

CRM Software – Life insurance coverage serves as a critical financial safeguard for individuals with dependents or outstanding financial obligations. The industry standard suggests coverage amounts typically range from 10 to 12 times an individual’s annual income, adjusted for specific debts such as mortgages, education costs, and final expenses. This calculation ensures that in the event of an untimely death, dependents and creditors are adequately supported without financial distress. Determining the precise amount requires a nuanced approach that considers multiple factors beyond income alone, including debt levels, future financial commitments, and available assets.

Choosing the right type of life insurance—term or permanent—also influences coverage strategy and premium costs. Term life insurance offers cost-effective protection over a specified period, ideal for covering temporary financial responsibilities such as a mortgage or child-rearing years. permanent life insurance extends coverage for life and accumulates cash value but comes with higher premiums. Timing the purchase of life insurance is equally important, as premiums escalate with age and health changes, making early acquisition advantageous. Regularly reassessing coverage aligns policies with evolving financial goals and life changes, avoiding underinsurance or overpayment.

Understanding Life Insurance Coverage Needs

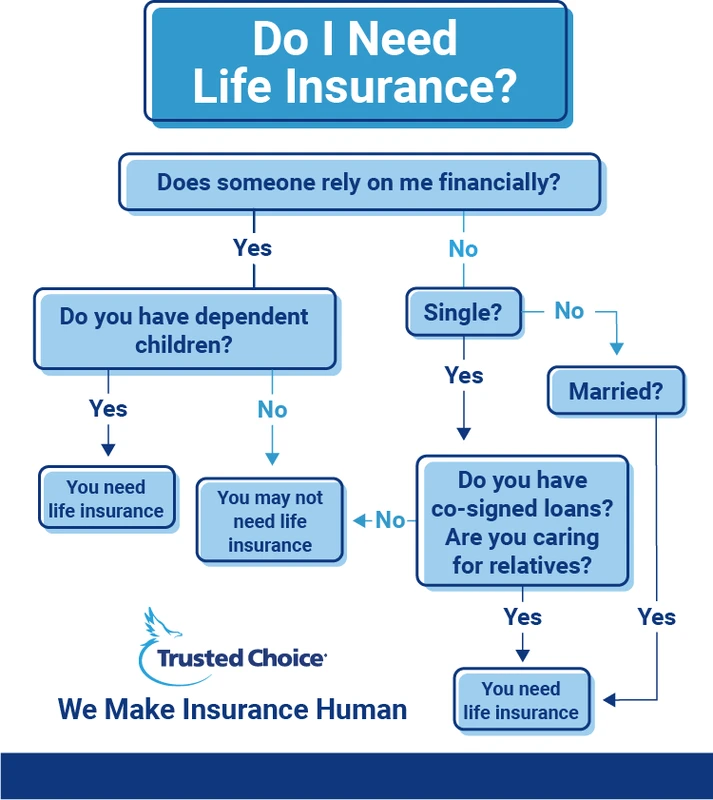

life insurance primarily functions as a financial safety net that replaces lost income and covers outstanding obligations when the insured passes away. It protects dependents who rely on the policyholder’s earnings, ensuring they can maintain their standard of living. Life insurance also covers debts that would otherwise become burdens for survivors, including mortgages, personal loans, and credit card balances. Beyond immediate family, life insurance provides for caregivers, small business owners (to fund business continuity), and can support charitable legacies.

Advertisement

Individuals most in need of life insurance include those with children, spouses, aging parents requiring care, or business partners. For example, a breadwinner with young children typically requires more coverage than a single person without dependents. Small business owners should consider life insurance to protect business continuity or buy-sell agreements. Those without financial dependents or substantial debts may not require extensive coverage, highlighting the importance of personalized assessment.

Key Factors Influencing Coverage Amount

Calculating appropriate life insurance coverage involves multiple variables. The most common starting point is income replacement, often estimated at 10 to 12 times annual income. This multiplier ensures that survivors receive sufficient funds to replace lost earnings over a typical working lifetime. However, this figure must be adjusted for outstanding debts and future financial commitments.

Mortgage payoff is a critical consideration, as it frequently represents the largest debt most families carry. Including the remaining mortgage balance in coverage ensures the home remains secure for survivors. Additionally, funding future expenses such as children’s education significantly impacts coverage needs. For instance, college tuition costs have risen sharply, with the average annual cost for a four-year public university exceeding $25,000, necessitating careful planning.

Final expenses, including funeral costs and medical bills, average around $15,000 to $20,000 and should be included to prevent survivors from incurring out-of-pocket expenses. Existing assets, such as savings, investments, and retirement accounts, reduce coverage needs; these resources can supplement life insurance payouts to meet financial obligations.

Types of Life Insurance and Impact on Coverage

term life insurance provides coverage for a set period—commonly 10, 20, or 30 years—offering affordable premiums tailored to cover temporary financial responsibilities. Term policies are ideal for covering periods when dependents are young or debts are high. However, coverage ends when the term expires, unless renewed, often at higher cost due to increased age and health risks.

Permanent life insurance, including whole and universal life policies, offers lifelong protection. These policies combine death benefits with a cash value component that grows over time, which policyholders can borrow against or use to pay premiums. While pricier than term insurance, permanent policies benefit individuals seeking long-term financial planning, estate tax advantages, or legacy creation.

Simplified issue life insurance allows for quick coverage approval without extensive medical exams, appealing to those with immediate coverage needs or health concerns. However, premiums tend to be higher, and coverage amounts lower compared to fully underwritten policies.

Calculating Your Life Insurance Coverage

The DIME method—Debt, Income, Mortgage, Education—is a practical framework for calculating life insurance needs. It involves summing outstanding debts, multiplying annual income by a factor (typically 10-12), adding mortgage balance, and estimating future education costs for children. This method provides a comprehensive snapshot of coverage requirements.

For example, consider a 35-year-old with an annual income of $75,000, a $200,000 mortgage, $50,000 in other debts, and two children expected to attend college. Using the DIME method:

Total recommended coverage: $750,000 + $200,000 + $50,000 + $100,000 = $1,100,000

Online life insurance calculators can refine this estimate by incorporating variables like age, health, asset values, and lifestyle. Consulting a financial advisor helps tailor coverage to individual circumstances, ensuring alignment with broader financial goals.

Timing and Reassessment of Life Insurance Coverage

Purchasing life insurance early locks in lower premiums, as age and health directly impact cost. Premiums typically increase substantially after age 50 or with the onset of chronic conditions. Buying coverage when young and healthy yields significant savings over time.

Life events such as marriage, birth of children, home purchase, or career changes necessitate reassessment of coverage. For instance, adding a child increases financial responsibilities, warranting higher coverage. Conversely, paying off a mortgage or children reaching financial independence may reduce needed coverage. Health improvements or declines also influence premium affordability and coverage adjustments.

Regular policy reviews every 3 to 5 years ensure coverage remains adequate and cost-effective. Some policies offer conversion options, allowing term policies to convert to permanent coverage without medical underwriting, providing flexibility as needs evolve.

When Life Insurance May Not Be Necessary

Life insurance may be unnecessary for individuals without dependents, significant debts, or financial obligations. For example, retirees with sufficient assets and no outstanding debts may opt to forgo life insurance. Similarly, individuals whose dependents are financially self-sufficient may require minimal coverage.

Alternatives to life insurance for financial planning include building emergency funds, investing in retirement accounts, or establishing trusts. However, these options do not replace the immediate liquidity and debt coverage life insurance provides upon death.

Practical Tips for Managing Premium Costs and Policy Selection

Age and health are primary determinants of life insurance premiums; younger, healthier applicants benefit from lower rates. Maintaining a healthy lifestyle and avoiding tobacco use enhance insurability. Selecting term lengths aligned with debt payoff horizons optimizes cost-effectiveness—for example, a 20-year term to cover a mortgage and child-rearing years.

Policy features such as renewability and conversion options add flexibility but may increase premiums. Evaluating these features against personal risk tolerance and financial goals is essential. Comparing quotes from multiple insurers and consulting financial advisors ensures informed decisions.

Life Insurance Type |

Coverage Duration |

Premium Cost |

Cash Value Component |

Best For |

|---|---|---|---|---|

Term Life Insurance |

10-30 years (fixed) |

Lower, affordable |

None |

Temporary needs, debt coverage |

Whole Life Insurance |

Lifelong |

Higher |

Yes, accumulates over time |

Long-term protection, estate planning |

Universal Life Insurance |

Lifelong, flexible |

Variable, adjustable |

Yes, flexible growth |

Flexible premiums, cash value growth |

Simplified Issue Life Insurance |

Varies |

Higher |

Usually none |

Quick coverage, limited underwriting |

This table summarizes key distinctions between life insurance types, assisting in matching policy choice with individual financial needs.

FAQ

How much life insurance coverage do I need?

Life insurance coverage is often recommended at 10 to 12 times your annual income, adjusted for debts like mortgages and future obligations such as education funding and final expenses. Using methods like the DIME formula helps tailor coverage to your financial situation.

What is the difference between term and permanent life insurance?

Term life insurance provides affordable coverage for a specified period, ideal for temporary needs, while permanent life insurance offers lifelong protection with a cash value component but comes with higher premiums.

When should I buy life insurance?

Purchasing life insurance early, while young and healthy, is advisable to secure lower premiums. Major life events such as marriage, having children, or purchasing a home are key times to buy or reassess coverage.

Can I adjust my life insurance coverage after purchase?

Yes, many policies allow adjustments, especially permanent policies with flexible premiums. Term policies often can be renewed or converted. Regular reassessment ensures your coverage aligns with changing financial goals.

Is life insurance necessary if I have no dependents?

Life insurance may not be essential if you have no dependents, debts, or financial obligations. In such cases, alternatives like savings or investments might suffice, but life insurance provides immediate financial liquidity upon death.

Life insurance remains a vital component of comprehensive financial planning, especially for those with dependents and substantial financial obligations. Understanding how to calculate appropriate coverage using methods like DIME, choosing the correct policy type, and timing your purchase strategically can optimize benefits and cost-efficiency. As financial circumstances evolve, proactive reassessment ensures your life insurance continues to meet your needs, protecting both your family’s future and your financial legacy.

For more detailed methodologies and personalized advice, consider consulting resources such as Fidelity’s Life Insurance Guide and Western Southern’s Life Insurance Analysis.

Advertisement