Advertisement

CRM Software – Term life insurance and whole life insurance represent two foundational types of life insurance policies, each designed around distinct financial goals, coverage needs, and premium structures. Term life insurance provides coverage for a predetermined period, such as 10, 20, or 30 years, with premiums typically lower than whole life policies but increasing upon renewal. In contrast, whole life insurance offers permanent coverage with fixed premiums and incorporates a cash value component that grows over time, serving both protection and investment purposes. Understanding the nuances between these policies is essential for policyholders aiming to align their insurance choice with budget constraints, estate planning objectives, and long-term financial strategies.

The choice between term and whole life insurance hinges on factors such as the desired coverage duration, cost sensitivity, and whether the policyholder values investment growth alongside death benefit protection. Term life insurance is generally recommended for those seeking affordable, temporary coverage to protect dependents during critical financial periods, like raising children or paying off a mortgage. Whole life insurance is favored by individuals needing lifelong coverage, estate preservation, and a policy that builds cash value to potentially borrow against or surrender for value later. Hybrid strategies combining both policy types can offer a tailored balance of affordability and lifelong protection, particularly for evolving financial circumstances.

Understanding Life Insurance: Term vs Whole Life

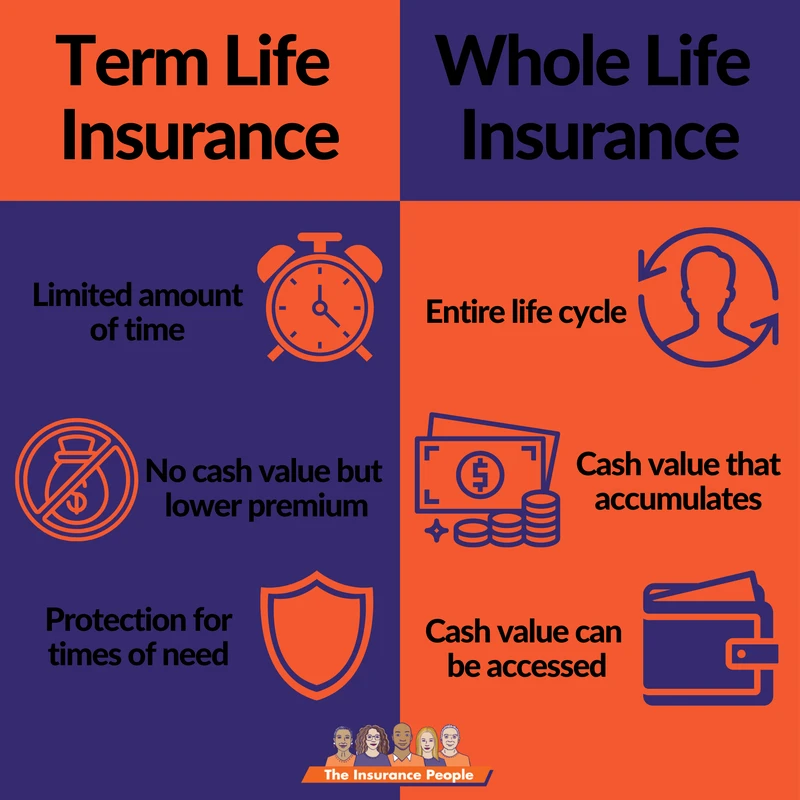

term life insurance is a straightforward product designed to provide financial protection over a specific period. If the insured passes away during the term, the policy pays out a death benefit to beneficiaries. However, if the term expires while the insured is still alive, no benefit is paid, and coverage ends unless the policy is renewed or converted. This type of insurance does not accumulate cash value, making it a pure risk protection product. The premiums are generally lower than whole life insurance at the outset but can increase significantly upon renewal, reflecting the insured’s advancing age and health status.

Advertisement

Whole life insurance, categorized under permanent life insurance, guarantees coverage for the insured’s entire lifetime as long as premiums are paid. It features fixed premiums and a guaranteed death benefit, alongside a cash value account that grows at a fixed or variable rate depending on the policy. This cash value serves as a savings component, accessible through policy loans or withdrawals, and can be surrendered for its accumulated value minus any surrender charges. The cash value growth is often tax-deferred, offering potential tax advantages for estate planning and wealth transfer.

Key Differences Between Term and Whole Life Insurance

Coverage duration is the most apparent distinction: term life insurance lasts for a defined term (commonly 10, 20, or 30 years), while whole life provides permanent coverage, typically until death. This permanent coverage guarantees a death benefit payout regardless of when the insured dies, unlike term insurance, which only pays if death occurs within the policy term.

Premium structure diverges significantly. Term life premiums start low and may rise with policy renewal, reflecting increased risk as the insured ages. Whole life premiums remain fixed throughout the policyholder’s life, offering predictable budgeting but at a higher initial cost. This fixed premium is partly allocated to funding the cash value component, which grows over time, providing an investment element absent in term policies.

Cash value accumulation is exclusive to whole life insurance. The cash value grows tax-deferred at a guaranteed or variable rate, depending on the insurer and policy type. Policyholders can borrow against this cash value, often at favorable interest rates, or surrender the policy to receive a lump sum minus any surrender fees. Dividends may be paid on participating whole life policies, representing the insurer’s surplus, which can be used to reduce premiums, buy additional coverage, or accumulate as cash.

The death benefit in term policies is a straightforward lump sum paid only if death occurs during the term. Whole life insurance guarantees a death benefit payout whenever the insured passes, making it suitable for estate planning and wealth transfer. Additionally, whole life death benefits may be enhanced through dividends or riders, offering more flexible coverage options.

Financial Implications and Cost Analysis

From a cost perspective, term life insurance is more affordable initially, making it accessible for younger individuals or families on a budget. However, premiums can escalate sharply with age or health changes upon renewal, which may pose challenges for long-term affordability. Whole life insurance demands higher premiums from the outset, but these fixed payments provide cost stability and lifelong coverage.

The cash value component in whole life policies provides financial flexibility. Policyholders can access accumulated cash through loans, which do not require credit checks but reduce the death benefit if unpaid. Surrendering the policy returns the cash value minus surrender charges, which can be substantial if done early in the policy. This liquidity feature enhances the policy’s utility as a financial asset, supplementing retirement planning or emergency funds.

Dividend-paying whole life policies add another dimension of potential growth. Though dividends are not guaranteed, many insurers consistently issue them based on their financial performance. Policyholders can reinvest dividends to increase cash value or reduce premiums, enhancing the policy’s overall value. Term life insurance does not offer dividends or cash value growth, focusing solely on death benefit protection during the term.

Choosing the Right Policy Based on Needs

Budget constraints strongly influence the choice between term and whole life insurance. Term life suits those requiring significant coverage for limited periods, such as covering a mortgage or funding children’s education, without the burden of high premiums. Whole life insurance is more suitable for individuals with stable incomes seeking to build permanent protection and accumulate wealth within the policy framework.

Coverage goals must be carefully assessed. For short-term financial responsibilities, term life insurance provides targeted protection without unnecessary expense. For long-term goals like estate planning, wealth transfer, or legacy building, whole life insurance offers advantages through permanent coverage and cash value growth. Whole life insurance also features tax advantages, as cash value growth and death benefits are generally tax-free, which can be critical for high-net-worth individuals.

Different life stages call for tailored recommendations. Young families often benefit from term life insurance due to affordability and coverage adequacy. Middle-aged individuals with accumulated assets may lean towards whole life or hybrid policies to integrate insurance with investment and estate planning strategies. Seniors typically evaluate the cost-benefit of whole life policies carefully, considering health status and the need for permanent coverage.

Hybrid and Alternative Life Insurance Options

Combining term and whole life insurance policies is an increasingly popular hybrid strategy. This approach allows policyholders to purchase affordable term insurance to cover immediate needs, supplemented by whole life insurance for permanent coverage and cash value accumulation. This combination can optimize premiums while maintaining lifelong protection.

Other permanent insurance types, such as universal life insurance, offer more flexibility in premium payments and death benefits, along with an investment component that varies with market performance. Universal life policies enable policyholders to adjust coverage amounts and premiums within contractual limits, aligning with changing financial goals. Variable life insurance is another alternative, offering investment choices within the policy but carrying higher risk.

These alternatives reflect the evolving landscape of life insurance products, providing policyholders with options to customize coverage and investment components according to their risk tolerance and financial objectives.

Practical Considerations and Common User Questions

When term life insurance expires, policyholders can often renew at higher premiums or convert the policy to a permanent form without medical underwriting, depending on the insurer’s terms. This conversion option provides a pathway to lifelong coverage if needs change.

Borrowing against whole life insurance cash value is a common financial strategy. Loans typically have low interest rates and no repayment schedule, but unpaid loans reduce the death benefit and cash value. Understanding loan mechanics is critical to avoid unintended reductions in coverage or policy lapse.

Evaluating the worth of whole life insurance involves assessing long-term financial goals, affordability, and the value of cash value growth versus pure protection. While whole life policies are more expensive, their dual role as insurance and investment can justify the cost for many, especially when integrated into comprehensive financial planning.

Life insurance needs evolve over time. Regular reviews of coverage amounts, policy features, and beneficiaries ensure alignment with current financial situations and goals. Consulting with financial advisors or insurance professionals can provide personalized recommendations and adjustments.

Aspect |

Term Life Insurance |

Whole Life Insurance |

Hybrid/Other Permanent Types |

|---|---|---|---|

Coverage Duration |

Fixed term (10, 20, 30 years) |

Lifetime coverage |

Flexible, permanent coverage |

Premiums |

Lower initial, may increase on renewal |

Fixed, higher initial cost |

Flexible (universal life), variable (variable life) |

Cash Value |

None |

Accumulates, accessible via loans/surrender |

Yes, varies by policy |

Death Benefit |

Paid if death occurs during term |

Guaranteed payout on death |

Guaranteed, adjustable |

Investment Component |

No |

Yes, fixed growth and dividends possible |

Yes, market-linked or fixed |

Best For |

Temporary protection, budget-conscious |

Permanent protection, estate planning |

Customized financial goals |

FAQ

What happens when term life insurance expires?

Term life insurance coverage ends at the end of the term. Policyholders can usually renew the policy at higher premiums or convert it to a permanent policy if conversion options exist, but no death benefit is paid if the insured outlives the term.

Can you borrow against whole life insurance cash value?

Yes, whole life policies accumulate cash value that policyholders can borrow against. Loans typically have low interest rates and no fixed repayment schedule, but any unpaid loan reduces the death benefit and cash value.

Are whole life insurance policies worth the cost?

Whole life insurance is worth the higher premiums if you need permanent coverage, value cash value accumulation, and want to use the policy for estate planning or as an investment vehicle. However, it may not suit those seeking low-cost, temporary coverage.

How do life insurance premiums compare between term and whole life?

Term life premiums are generally lower initially but can increase significantly upon renewal. Whole life premiums are higher but fixed for life, providing predictable payments and lifelong coverage.

What are the tax implications of whole life insurance?

Cash value growth in whole life policies is tax-deferred, and death benefits are generally paid out income-tax-free to beneficiaries, making whole life insurance advantageous for estate planning and wealth transfer.

For more detailed information on life insurance types and cost comparisons, visit Progressive’s guide on term vs whole life insurance and Investopedia’s comprehensive analysis.

Choosing between term and whole life insurance requires a careful assessment of your financial goals, coverage needs, and budget. As life circumstances evolve, hybrid policies and flexible permanent insurance products offer opportunities to tailor protection and investment components dynamically. Consulting with insurance professionals to periodically review and adjust your coverage ensures your life insurance aligns with your changing financial landscape and estate planning objectives.

Advertisement