Advertisement

CRM Software – Insurance claims are rejected primarily due to incomplete or inaccurate documentation, policy exclusions, delayed reporting, or services deemed not medically necessary. These reasons span across health, auto, homeowners, business, and disability insurance policies. For policyholders facing denial, understanding the specific cause cited by insurers—often detailed in a denial letter—is critical. Successful appeals require systematic evidence gathering, including medical records, police reports, or proof of timely submission. Consulting legal experts or specialized attorneys familiar with insurance law can substantially increase the chance of overturning unjust denials, especially in complex cases involving long-term disability or health claims.

Insurance companies, claims adjusters, and third-party administrators (TPAs) play pivotal roles in evaluating claims. Regulatory bodies such as the Employee Benefits Security Administration (EBSA) oversee fair practices and enforce appeal rights. Independent Review Organizations (IROs) provide external evaluations when internal appeals are exhausted. Together, these entities influence the claims landscape, which has seen rising denial rates in recent years due to changing medical coding guidelines and stricter policy interpretations.

Understanding Insurance Claim Rejection

insurance claim rejection occurs when an insurer refuses payment on a submitted claim, often citing specific reasons in a denial letter. Denials affect all common insurance types including health, auto, homeowners, business, renter’s, and long-term disability insurance. The most frequent causes include incomplete documentation, policy exclusions, and delayed claim reporting.

Advertisement

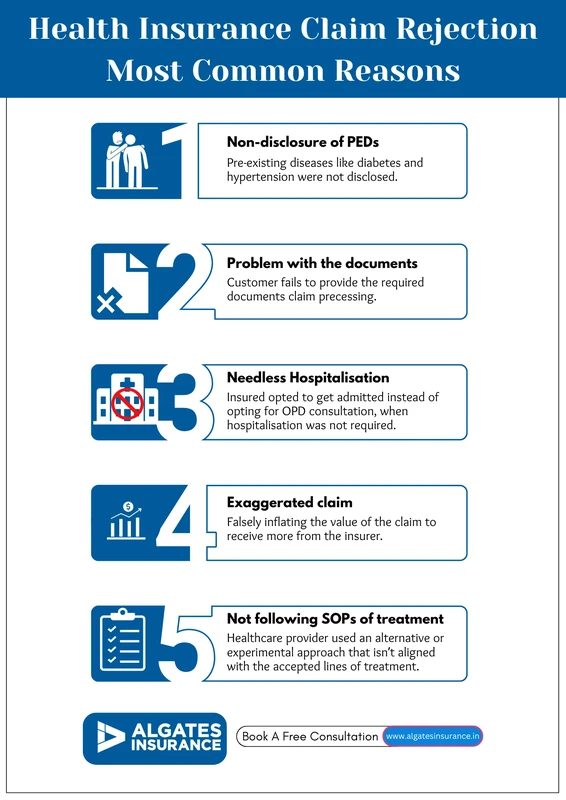

For example, health insurance claims are frequently denied due to failure to meet medical necessity criteria, a core coverage condition insurers use to limit payment to treatments deemed essential. Auto insurance claims often face rejection due to late accident reporting or lack of police reports. Homeowners insurance denials commonly arise from policy exclusions related to certain types of damage or incidents, such as flooding or wear and tear. Long-term disability claims may be rejected due to insufficient evidence of disability severity or non-compliance with medical coding guidelines.

Policy exclusions significantly impact claim outcomes. Many insurance contracts explicitly exclude coverage for pre-existing conditions, elective procedures, or specific perils, which means claims related to these are systematically denied. Delayed reporting also plays a crucial role; insurers require claims to be filed within a set timeframe, typically 30 to 90 days post-incident. Failure to comply often results in automatic rejection regardless of claim validity.

Typical Documentation and Coverage Issues Leading to Denials

Incomplete or inaccurate documentation remains the leading cause of claim denial across all insurance segments. Common errors include missing signatures, illegible forms, inaccurate policy numbers, and incomplete medical records. These documentation flaws prevent claims adjusters from verifying eligibility and service details, prompting outright rejection.

insurance coverage lapses, such as unpaid premiums or policy cancellations, also lead to denials. Many policyholders are unaware that their coverage status affects claim acceptance, particularly with health and auto insurance where continuous coverage is essential. Non-covered services—those explicitly excluded in the policy—are another frequent denial cause. Insurers may deny claims for procedures deemed experimental, cosmetic, or outside the agreed scope.

Medical necessity denials are specific to health and disability insurance. Insurers apply internal policies and external medical coding guidelines—such as those updated in 2024—to evaluate if a treatment is warranted. The Kaiser Family Foundation reports a 60% increase in denial rates linked to recent medical coding changes, reflecting insurers’ heightened scrutiny. For instance, treatments not aligning with current procedural codes or lacking evidence-based justification are commonly rejected.

Navigating the Appeals Process

When a claim is denied, the insurer must provide a written denial notice detailing the reasons and outlining the appeals process. Policyholders should first carefully review this denial letter to understand the specific grounds for rejection.

Successful appeals require gathering comprehensive evidence to counter denial reasons. This includes obtaining complete medical records, police or accident reports, billing statements, and correspondence. Consulting healthcare providers or medical coders can help clarify documentation to meet insurer requirements.

A strong appeal letter should explicitly address each denial reason, provide supporting documentation, and cite policy language or medical necessity criteria where applicable. Timeliness is critical; most insurers impose strict deadlines—often 30 to 60 days—for submitting appeals.

Third-party administrators (TPAs) often handle the initial appeals process on behalf of insurers. Policyholders can also seek assistance from regulatory bodies like the Employee Benefits Security Administration (EBSA), which can intervene in ERISA-governed health plans to ensure compliance with federal appeal rights. In some cases, escalating the appeal to an Independent Review Organization (IRO) is possible if the insurer denies the internal appeal.

Legal and Expert Support in Claim Denials

Certain claim denials, particularly those involving substantial sums or complex policies like long-term disability, warrant legal consultation. Insurance attorneys specialize in interpreting policy terms, identifying procedural errors, and advocating for policyholders in disputes.

Timely notice to the insurer and adherence to appeal deadlines are essential to preserve legal rights. Failure to appeal within specified timeframes can forfeit the chance to contest the denial.

Senior claims analysts and Disability Management Units within insurance companies play a role in re-evaluating complex or disputed claims. Their involvement can lead to reversals if new evidence or clarifications emerge.

When internal appeals fail, Independent Review Organizations (IROs) offer an impartial external review. The IRO examines medical necessity and policy adherence independently, often resulting in higher overturn rates for denied health and disability claims.

Preventing Future Claim Rejections

Proactive measures significantly reduce denial risks. Best practices include meticulous documentation and prompt reporting of incidents or medical services. Verify insurance coverage and policy terms before incurring expenses, especially for elective or complex procedures.

Providers and policyholders should communicate openly about policy limitations and exclusions to manage expectations and avoid surprises. Training on accurate medical coding and billing is essential to comply with evolving insurer requirements.

Regular audits and claims reviews can identify patterns of rejection, enabling corrective action. For example, revising documentation templates or improving patient education can mitigate common errors.

Case Studies and Trends

Denial rates have escalated notably in recent years, driven by stricter insurer policies and evolving medical coding standards. According to the Kaiser Family Foundation, less than 1% of denied patients appeal, but over 50% of those appeals succeed, highlighting the importance of pursuing recourse.

In health insurance, updated coding guidelines introduced in 2024 have resulted in a 60% increase in claim denials among medical groups, reflecting insurer efforts to contain costs and prevent fraud. Long-term disability claim appeals have also increased as claimants navigate more rigorous documentation demands.

Successful appeals often involve detailed medical evidence and legal advocacy. For instance, Sun Life Assurance Company reported several cases where appeals reversed initial denials after submission of additional documentation verifying disability severity and compliance with policy terms.

Insurance Type |

Common Denial Reasons |

Appeal Success Rate |

Key Entities Involved |

|---|---|---|---|

Health Insurance |

Medical necessity, coding errors, policy exclusions |

50%+ (Kaiser Foundation data) |

Claims adjusters, IROs, EBSA |

Auto Insurance |

Delayed reporting, insufficient evidence, policy lapses |

30-40% |

Claims adjusters, TPAs |

Homeowners Insurance |

Exclusions (flood, wear & tear), incomplete claims |

25-35% |

Claims adjusters, third-party evaluators |

Long-Term Disability |

Insufficient medical documentation, policy limitations |

40-50% |

Disability Management Units, attorneys, IROs |

FAQ

Why do insurance claims get rejected?

Insurance claims are most commonly rejected due to incomplete or inaccurate documentation, policy exclusions, late claim reporting, or services not meeting medical necessity criteria. Each insurance type has specific reasons, such as coding errors in health claims or delayed accident reports in auto insurance.

How can I appeal a denied insurance claim?

To appeal, first obtain the insurer’s denial letter and understand the reasons. Gather all supporting evidence like medical records or police reports, write a detailed appeal letter addressing each denial reason, and submit within the insurer’s deadline. Consulting an attorney or regulatory agencies like EBSA can improve appeal outcomes.

What role do Independent Review Organizations (IROs) play in the appeal process?

IROs provide an impartial external review when insurers deny internal appeals. They reassess medical necessity and policy compliance independently, often increasing the chances of overturning denials, especially in health and disability claims.

Are there statistics on how often appeals succeed?

Yes, according to the Kaiser Family Foundation, over 50% of appealed health insurance claim denials are overturned. However, fewer than 1% of denied claimants actually file appeals, indicating significant opportunities for recourse.

When should I consult an attorney for a denied insurance claim?

Legal consultation is recommended for complex claims, large sums, or repeated denials. Attorneys specializing in insurance law can identify procedural errors, help gather evidence, meet appeal deadlines, and represent claimants in disputes or litigation.

Insurance claims denial involves multiple factors, from documentation errors to policy terms and evolving coding standards. Navigating this landscape requires detailed understanding of insurer requirements, diligent evidence collection, and knowledge of appeal rights. As denial rates rise, policyholders benefit from proactive documentation practices, timely appeals, and expert legal support. Future trends suggest increasing insurer scrutiny, making early legal and regulatory intervention more critical to successful claim resolution.

For further detailed guidance on insurance claim denials and appeals, visit Western Financial Group’s insurance claim denial resource and Healthline’s insurance appeal guide.

Advertisement