Advertisement

CRM Software – Car insurance constitutes a legally mandated financial safety net designed to protect drivers from the potentially devastating costs associated with vehicle-related accidents. In Canada, this coverage primarily safeguards against liabilities arising from injuries or property damage inflicted on others, while also offering optional protections for the insured’s own vehicle and related expenses. The foundational component of car insurance is liability coverage, which is compulsory across Canadian provinces and territories, though minimum coverage amounts and regulatory frameworks differ regionally. Beyond liability, drivers can opt for collision coverage, which addresses damages from at-fault accidents, and comprehensive coverage, which protects against non-collision risks such as theft, vandalism, or adverse weather events.

A distinctive feature in most Canadian jurisdictions is Direct Compensation Property Damage (DCPD), a mechanism that streamlines claims by allowing drivers to seek vehicle repairs through their own insurer when they are not at fault. This contrasts with traditional tort-based claims processes and significantly reduces administrative burdens. Additionally, accident benefits provide critical support that covers medical expenses, rehabilitation costs, income loss, and in severe cases, death benefits, ensuring financial protection beyond vehicle repair. Premiums, the recurring payments drivers make for coverage, are influenced by a complex matrix of factors including age, driving history, vehicle type, and regional risk assessments. Deductibles, chosen at policy inception, dictate the out-of-pocket expense when filing a claim and are a strategic consideration balancing upfront costs and claim affordability.

Mandatory vs Optional Coverage in Canadian Car Insurance

Canadian provinces uniformly require drivers to hold liability insurance, yet the scope and minimum limits vary. Liability coverage compensates third parties for bodily injury and property damage resulting from the insured driver’s negligence. For example, Ontario mandates a minimum of $200,000 in liability coverage, while Alberta requires $200,000 but recommends higher limits to accommodate inflation and litigation trends. This mandatory coverage ensures drivers can meet legal obligations following an accident and protects victims from uncompensated losses.

Advertisement

Optional coverages expand protection beyond legal minimums. collision coverage reimburses for damages to the policyholder’s vehicle resulting from collisions, irrespective of fault. Comprehensive coverage addresses risks such as theft, fire, vandalism, and natural disasters, essential safeguards in urban areas prone to vehicle theft or rural regions exposed to wildlife or weather damage. Rental car coverage facilitates temporary vehicle replacement during repair periods, maintaining driver mobility without additional out-of-pocket expenses. Uninsured motorist coverage protects drivers when involved in accidents caused by uninsured or hit-and-run offenders, a critical layer given that uninsured driving rates vary across provinces. These optional coverages offer tailored protection, allowing drivers to adapt policies to their risk tolerance and financial situation.

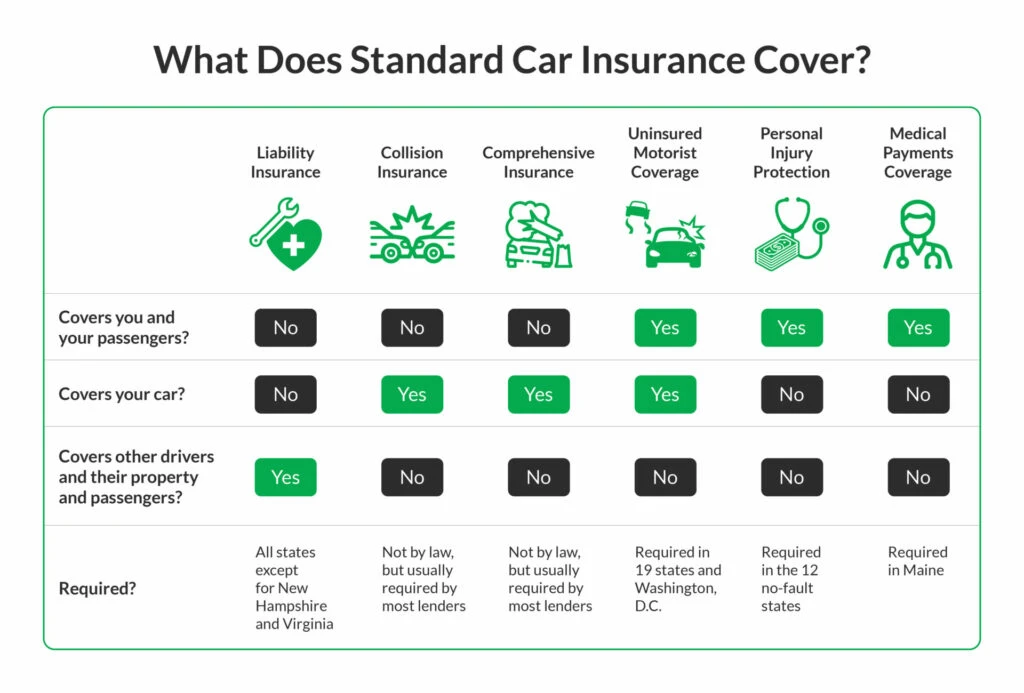

Detailed Types of Car Insurance Coverage

<liability coverage is the backbone of any policy, encompassing both bodily injury and property damage liability. It legally obligates insurers to pay claims up to policy limits for injuries or property damage the insured driver causes to others. For instance, if a driver causes a collision resulting in another person’s hospital bills and vehicle repair costs, liability insurance covers these expenses. However, it excludes damages to the insured’s own vehicle, underscoring the need for additional coverage.

Collision coverage specifically addresses damages to the insured vehicle caused by collisions with other vehicles or objects. It is particularly valuable for drivers with newer or higher-value cars, where repair costs can be substantial. For example, a collision with a guardrail or another car would be covered under this policy component, subject to the deductible.

Comprehensive coverage protects against non-collision risks, which can vary widely but often include theft, vandalism, hail damage, flooding, and animal strikes. For example, drivers in areas with frequent hailstorms or high theft rates benefit significantly from comprehensive coverage, as repair or replacement costs from these incidents can be unexpectedly high.

Rental car coverage reimburses the costs of renting a vehicle while the insured’s car undergoes repairs due to a covered claim. This coverage is particularly useful when repair timelines extend over several days or weeks, enabling uninterrupted mobility. Not all policies include this automatically, so drivers must verify and opt in if desired.

Accident benefits cover medical and rehabilitation expenses, income replacement, and death benefits regardless of fault, providing a crucial safety net for personal injury protection. These benefits vary by province but typically include coverage for hospital stays, therapy, and compensation for lost wages due to injury.

Direct Compensation Property Damage (DCPD) is unique to Canadian insurance and applies in provinces like Ontario, Quebec, and Manitoba. It allows insured drivers to file claims for vehicle damage through their own insurer when not at fault, reducing delays and disputes common in fault-based claims. This system expedites repairs and simplifies the legal process, benefiting both insured drivers and insurers.

Factors Influencing Premiums and Deductibles

insurance premiums are calculated based on a broad range of personal and vehicle-specific factors, many of which are under the driver’s control. Age is a significant determinant; younger drivers typically face higher premiums due to statistically higher accident rates. Gender may influence rates, with some insurers charging more for males in certain age brackets, though regulatory scrutiny on this practice varies. Driving history is critical; a clean record with no claims or violations can substantially lower premiums, whereas accidents or infractions often cause significant rate increases.

The vehicle’s make, model, and year also impact premiums. High-performance or luxury cars generally attract higher rates due to increased repair costs and theft risk. Usage patterns, such as annual mileage and primary use (commuting vs recreational), influence risk assessments. Geographical location affects premiums because urban areas tend to have higher rates of accidents, theft, and vandalism compared to rural regions.

Deductibles, the amount paid out-of-pocket before insurance coverage applies, are customizable. Higher deductibles lower premiums but increase financial risk in the event of a claim. Selecting an appropriate deductible involves balancing affordable premium payments against potential claim costs, with many insurers offering deductible options ranging from $500 to $2,500.

Choosing the Right Car Insurance Coverage

Determining the optimal car insurance coverage requires evaluating vehicle value, personal financial situation, and risk tolerance. For newer vehicles, collision and comprehensive coverages are usually prudent, given the high repair or replacement costs. Conversely, for older or low-value cars, the cost of additional coverage might exceed the benefit, prompting some drivers to opt for liability-only policies.

Assessing personal risk tolerance involves considering driving environments, frequency, and historical accident data. For example, drivers in high-traffic metropolitan areas or those who frequently travel may prioritize comprehensive and rental car coverage, while infrequent drivers in low-risk regions might minimize coverage to reduce premiums.

Understanding policy specifics is vital. Drivers should scrutinize coverage limits, exclusions, and claim procedures. For instance, some policies exclude certain weather-related damages or require additional riders for rental car coverage. Transparent communication with insurance providers and comparison of quotes from multiple companies, such as Intact, belairdirect, or TD Insurance, can reveal better rates and more suitable coverage options.

Legal Consequences of Driving Uninsured in Canada

Driving without insurance in Canada carries severe legal penalties, reflecting the societal imperative to protect all road users. Consequences include substantial fines, which vary by province but can reach several thousand dollars. License suspensions and vehicle impoundments are common, disrupting personal and professional mobility.

Moreover, uninsured drivers face financial liability for all damages and injuries they cause, exposing them to lawsuits and significant out-of-pocket expenses. Insurance providers classify uninsured drivers as high-risk, resulting in steep premium increases upon future coverage acquisition. Some provinces impose additional administrative penalties and may require mandatory financial responsibility filings before reinstating driving privileges.

Understanding the Car Insurance Claims Process

Filing a claim after a vehicle accident initiates a structured process designed to assess damages, determine fault, and facilitate repairs or compensation. In at-fault scenarios, drivers file claims with their own insurer for collision coverage, while liability claims address damages to third parties. Not-at-fault drivers benefit from DCPD, allowing claims through their insurer without involving the at-fault party’s insurer directly.

Comprehensive claims cover non-collision damages, often requiring police reports or third-party verification, especially for theft or vandalism. Timely reporting is critical; most insurers mandate notification within a specified time window, commonly 7 to 14 days post-incident.

Documentation strengthens claims. Photographs, witness statements, police reports, and repair estimates support accurate damage assessments. Insurers may appoint adjusters who inspect vehicles and verify claims before authorizing repairs or payouts. Deductibles apply per policy terms, and unresolved disputes can escalate to arbitration or legal proceedings.

Frequently Asked Questions (FAQs)

What happens if I cause an accident but only have liability coverage?

Liability coverage will pay for injuries and property damage suffered by others, but it does not cover damage to your own vehicle. You would be responsible for repair or replacement costs yourself, which could be financially burdensome depending on the severity of the accident.

Is rental car coverage worth adding to my policy?

Rental car coverage provides reimbursement for temporary transportation costs while your vehicle is being repaired after a covered claim. It is particularly valuable if you rely heavily on your vehicle daily and cannot afford downtime. Without it, you must pay rental costs out of pocket or arrange alternative transportation.

How can I reduce my car insurance premiums?

Maintaining a clean driving record, choosing higher deductibles, bundling policies (e.g., home and auto), and selecting vehicles with lower risk profiles can reduce premiums. Additionally, some insurers offer discounts for safety features, low annual mileage, and driver training programs.

Does a clean driving record really lower my insurance rates?

Yes, insurers reward safe driving with lower premiums, as it statistically correlates with reduced claim likelihood. Conversely, accidents and violations increase risk profiles, leading to higher rates.

Are red cars more expensive to insure?

This is a common myth. Insurance premiums are based on risk factors such as driver history, vehicle type, and location, not the color of the car. Red cars do not inherently attract higher insurance costs.

—

Looking ahead, the evolving landscape of car insurance in Canada is shaped by emerging technologies such as telematics and AI-driven risk assessments, which promise more personalized, dynamic premium calculations. Drivers can expect greater transparency and options to customize coverage based on real-time driving behavior. Additionally, regulatory bodies continue refining frameworks to balance consumer protection with affordability, especially in high-risk urban areas. Understanding the nuances of coverage types, provincial legal requirements, and claims processes empowers drivers to make informed decisions, ensuring financial security and compliance on Canadian roads.

For further detailed guidance on auto insurance coverage and regulations, consult the Insurance Bureau of Canada’s official auto insurance resource and explore coverage options with major providers such as belairdirect’s auto coverage guide.

Advertisement