Advertisement

CRM Software – Life insurance offers a critical financial safety net by providing a tax-free death benefit to beneficiaries. This benefit replaces lost income, covers outstanding debts such as mortgages, pays final expenses, and can help manage estate taxes. In Canada, death benefits from most life insurance policies are exempt from income tax, ensuring that beneficiaries receive the full payout. The two primary types of life insurance—term and whole life—serve distinct financial needs. Term life insurance provides affordable, fixed-duration coverage, often used for income replacement or mortgage protection. Whole life insurance guarantees lifelong coverage with a death benefit payout and accumulates cash value that policyholders can access during their lifetime for retirement income or emergencies.

Whole life and other permanent life insurance policies, including participating whole life and universal life, incorporate a savings component, allowing dividends or interest to build cash value. This cash value can be borrowed against or withdrawn, offering flexibility that term policies lack. Policyholders can also add riders—customizable features that enhance coverage—such as accelerated death benefits, which provide funds if a critical illness diagnosis occurs, or critical illness coverage riders that pay out on diagnosis of specified conditions. These features tailor life insurance to evolving personal circumstances and financial goals.

Types of Life Insurance and Their Unique Advantages

Term life insurance is popular due to its affordability and simplicity. Premiums remain fixed during the term, which typically ranges from 10 to 30 years, making it a practical choice for covering temporary financial responsibilities like raising children or paying off a mortgage. Term policies are renewable and often convertible to permanent insurance without new medical underwriting, offering flexibility if long-term coverage becomes necessary. However, term insurance does not build cash value and expires if the insured outlives the term.

Advertisement

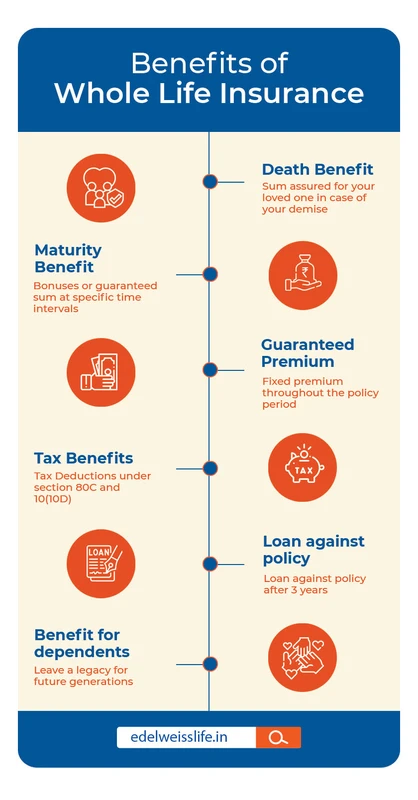

whole life insurance provides guaranteed lifelong protection, with premiums generally higher than term insurance but remaining level throughout the policyholder’s life. The cash value component grows tax-deferred and can be accessed through loans or withdrawals, providing an alternative income source during retirement or financial hardship. Participating whole life policies pay dividends, which policyholders can use to reduce premiums, increase death benefits, or accumulate additional cash value. Universal life insurance offers a more flexible premium structure and adjustable death benefits, appealing to those with changing financial circumstances.

Other options like guaranteed acceptance life insurance require no medical exam and provide coverage regardless of health, though premiums are considerably higher and death benefits lower. These policies are often used for final expense coverage or for individuals with health concerns who may not qualify for traditional policies.

Financial Benefits Beyond the Death Benefit

Life insurance serves as a foundational element of financial planning by replacing lost income for dependents, ensuring the family’s financial stability after the policyholder’s death. It covers funeral expenses, outstanding debts—including mortgages, credit cards, and personal loans—and can prevent beneficiaries from liquidating assets under unfavorable conditions. In estate planning, life insurance provides liquidity to cover inheritance taxes and probate fees, enabling smoother asset transfer to heirs without forced sales.

cash value in permanent policies offers a living benefit, allowing policyholders to borrow against their insurance for major expenses or supplement retirement income. This can be particularly advantageous in tax planning, as policy loans are generally tax-free if managed properly. Dividend payments from participating whole life policies represent another financial benefit; though not guaranteed, they can enhance overall returns and reduce out-of-pocket premium costs.

Policy Features and Riders: Enhancing Coverage Flexibility

Riders expand the scope of life insurance, adapting it to specific needs. The accelerated death benefit rider allows access to a portion of the death benefit if diagnosed with a terminal illness, providing funds for medical care or other expenses. Critical illness riders pay out upon diagnosis of severe health conditions, such as cancer or stroke, offering financial relief during treatment. Disability waiver of premium riders ensure the policy remains active if the insured becomes disabled and cannot work.

Other riders include child term riders, which provide coverage for children, and guaranteed insurability riders that allow policyholders to increase coverage without medical exams at specified life events, such as marriage or the birth of a child. These add-ons enhance protection and provide peace of mind by addressing unforeseen life changes.

Life Insurance in Context: Homeowners, Employees, and Business Owners

Homeowners often benefit from decreasing term life insurance, which aligns coverage with the declining mortgage balance. This ensures that the outstanding loan is covered if the insured dies before the mortgage is paid off, protecting the family home. In workplace settings, group life insurance is a common employee benefit, but it typically offers limited coverage. Employees frequently need supplemental individual life insurance to meet their full financial needs.

Business owners use life insurance for various strategic purposes, including key person insurance, which protects the company against financial losses caused by the death of a vital employee. Buy-sell agreements funded by life insurance facilitate business continuity by providing liquidity to buy out deceased partners’ shares. Additionally, naming charities as beneficiaries allows policyholders to leave a philanthropic legacy with tax advantages.

Claims Process and Importance of Beneficiary Designations

The claims process for life insurance generally involves submitting a death certificate and claim form, with payouts typically occurring within weeks if documentation is complete. Life insurance proceeds usually bypass probate, expediting access for beneficiaries and minimizing legal fees. Maintaining up-to-date beneficiary designations is crucial to avoid delays or disputes; changes in personal circumstances like marriage, divorce, or the birth of children should prompt policy reviews.

Insurers provide support throughout the claims process, and transparency in communication helps beneficiaries understand their rights and timelines. Beneficiaries can receive the death benefit as a lump sum or in installments, depending on policy terms and personal preference.

Choosing the Right Life Insurance: Factors to Consider

Premium costs depend on factors such as age, health, coverage amount, and policy type. Term insurance offers lower initial premiums but may become more expensive upon renewal or conversion. Whole life premiums are higher but fixed, providing budget predictability. Policy duration and renewal options should align with financial responsibilities and long-term goals.

Consulting with a financial adviser helps tailor life insurance choices based on individual circumstances, including estate planning objectives, tax considerations, and retirement strategies. Professional advice ensures the selected policy maximizes benefits while fitting within the broader financial plan.

Life Insurance Type |

Coverage Duration |

Premiums |

Cash Value |

Key Benefits |

|---|---|---|---|---|

Term Life Insurance |

Fixed term (10-30 years) |

Lower, fixed during term |

No |

Affordable, income replacement, mortgage protection |

Whole Life Insurance |

Lifelong |

Higher, fixed |

Yes, accumulates cash value |

Guaranteed payout, dividends, cash value loans |

Universal Life Insurance |

Lifelong with flexible terms |

Flexible premiums |

Yes, with adjustable death benefit |

Flexible coverage and premiums |

Guaranteed Acceptance Life |

Lifelong |

Highest |

No or minimal |

No medical exam, final expense coverage |

This table summarizes core differences among major life insurance types, illustrating how each fits distinct financial roles.

FAQ

What are the main benefits of life insurance?

Life insurance provides a tax-free death benefit that replaces lost income, covers debts, funeral expenses, and estate taxes. Permanent policies also build cash value usable during the insured’s lifetime.

How does whole life insurance differ from term life insurance?

Whole life insurance offers lifelong coverage with fixed premiums and cash value accumulation, while term life insurance provides coverage for a set period with lower premiums but no cash value.

Can life insurance help with estate planning?

Yes, life insurance provides liquidity to pay estate taxes and avoid probate delays, ensuring assets transfer smoothly to heirs.

What are policy riders and how do they enhance coverage?

Riders are optional add-ons like accelerated death benefits or critical illness coverage that increase a policy’s flexibility and protection based on individual needs.

How important is beneficiary designation?

Keeping beneficiary information current is crucial to ensure timely payout and avoid legal complications after the insured’s death.

Selecting the appropriate life insurance involves balancing cost, coverage duration, and financial goals. With evolving products and policy riders, life insurance remains a versatile tool for securing financial futures, supporting estate plans, and protecting businesses. Consulting trusted providers such as Legal & General’s life insurance guides or RBC Insurance’s expert advice can help navigate options for optimal policy selection and management.

Advertisement