Advertisement

CRM Software – Life insurance is a financial contract between an individual—the policyholder—and an insurance company, designed to provide a tax-free death benefit to designated beneficiaries upon the insured’s death. This benefit serves various financial purposes such as covering funeral costs, paying off debts, replacing lost income, or supporting long-term financial planning goals. Life insurance products primarily fall into two categories: term life insurance, which offers coverage for a predetermined period, and permanent life insurance, which provides lifelong protection with the added advantage of cash value accumulation.

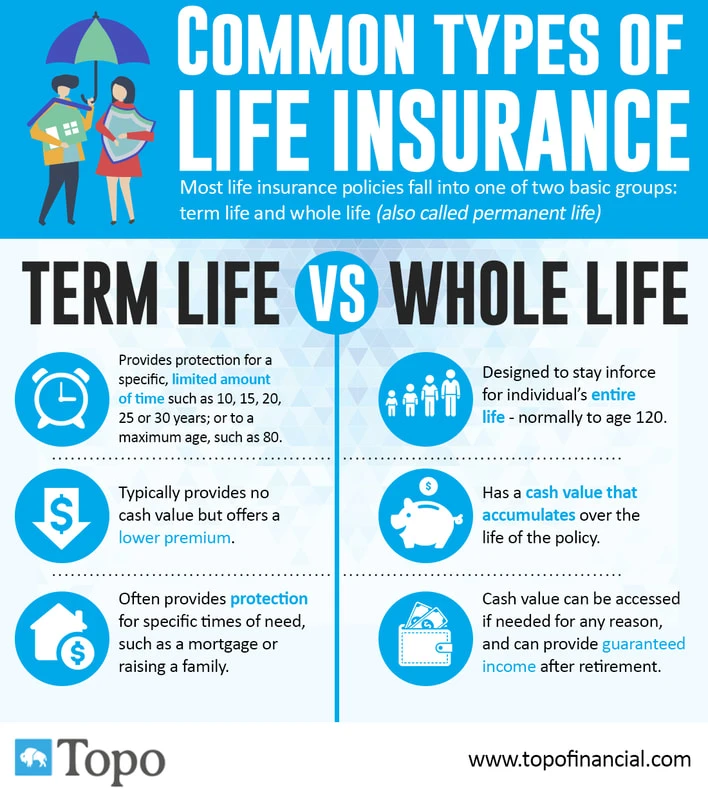

Term life insurance typically covers durations ranging from one to thirty years and pays out only if the insured passes away within that term. In contrast, permanent life insurance, including whole life and universal life policies, guarantees coverage for the insured’s entire lifetime, often blending protection with an investment component that builds cash value over time. The distinction between these types influences premium costs, policy features, and suitability for different financial objectives. Understanding these fundamentals is essential for selecting appropriate coverage that aligns with personal financial needs and life circumstances.

Understanding Life Insurance: Definition and Purpose

Life insurance is fundamentally a risk management tool that transfers the financial burden of premature death from the policyholder to the insurance company. Beyond the death benefit, it plays a crucial role in comprehensive financial planning by ensuring that dependents and obligations are protected. Policyholders pay premiums—usually monthly or annually—in exchange for this coverage.

Advertisement

The beneficiaries, individuals or entities designated by the policyholder, receive the death benefit tax-free, which can be strategically used to cover outstanding debts such as mortgages, education expenses, or daily living costs. Insurable interest, a legal prerequisite, mandates that the policyholder must have a legitimate financial interest in the insured person’s life, ensuring the purpose of the insurance aligns with genuine economic loss prevention.

Life insurance benefits a broad spectrum of individuals: young families seeking income replacement, homeowners aiming to secure mortgage obligations, business owners managing succession risks, and retirees addressing estate planning needs. For instance, a young couple purchasing term life insurance to protect against income loss during child-rearing years exemplifies practical insurance use.

Types of Life Insurance

Term Life Insurance

Term life insurance provides coverage for a specific period, often ranging from 1 to 30 years. Its primary appeal lies in affordability and simplicity, offering a straightforward death benefit without cash value accumulation. There are two main structures within term life: level term and decreasing term.

Level term insurance maintains a constant death benefit and premium throughout the term, making it ideal for those requiring stable coverage, such as young families protecting income until children reach adulthood. Decreasing term insurance reduces the death benefit gradually, commonly aligned with declining liabilities like mortgage balances.

Renewal and conversion options vary by policy but generally allow policyholders to renew coverage after the term expires or convert term insurance into a permanent policy without undergoing new medical exams. However, premiums typically increase upon renewal due to age and health changes. In Canada, providers like Canada Life and RBC Insurance offer flexible term life products with conversion features, catering to evolving financial needs.

Permanent Life Insurance

Permanent life insurance encompasses whole life and universal life policies, designed to provide lifelong coverage. Whole life insurance features fixed premiums, a guaranteed death benefit, and builds cash value at a predetermined rate. The cash value grows tax-deferred and can be accessed through loans or withdrawals, providing a financial resource during the policyholder’s lifetime.

Universal life insurance offers more flexibility, allowing adjustments to premiums and death benefits within policy limits. It also accumulates cash value based on credited interest rates or investment performance, depending on the policy type (e.g., indexed universal life). Participating whole life policies pay dividends to policyholders, which can be used to reduce premiums or increase cash value.

The higher premiums associated with permanent insurance reflect its dual role as protection and a financial asset. These policies can be integral to estate planning, providing liquidity for tax obligations or wealth transfer. Sun Life, a major player in the Canadian market, emphasizes universal life products for clients seeking customizable coverage with investment components.

How Life Insurance Works

A life insurance policy involves three key parties: the policyholder, the insured, and the beneficiary. The policyholder owns the contract and is responsible for premium payments. The insured is the individual whose life is covered, and the beneficiary is the recipient of the death benefit.

Premiums are calculated based on actuarial risk assessments, considering factors such as age, health status, lifestyle choices (e.g., smoking), and the coverage amount. Younger, healthier individuals typically enjoy lower premiums. Insurance companies underwrite policies to price risk accurately, balancing competitive pricing with long-term sustainability.

Upon the insured’s death, the beneficiary files a claim with the insurance company, which verifies the policy status and circumstances of death. Provided all conditions are met, the insurer pays the death benefit as a lump sum, free from income tax in most jurisdictions. This payout can significantly ease financial burdens during bereavement.

Legal concepts such as insurable interest ensure policies are not exploited for speculative purposes. Insurable interest must exist at the policy’s inception, meaning the policyholder must demonstrate a financial stake in the insured’s continued life. This requirement protects against moral hazard and fraud.

Determining How Much Life Insurance You Need

Calculating the appropriate coverage amount requires a detailed assessment of financial obligations and goals. Key factors include current and future income replacement needs, outstanding debts like mortgages and loans, ongoing living expenses for dependents, and anticipated costs such as education or funeral expenses.

Financial advisors and insurance companies provide calculators to estimate coverage, often using methods like the “DIME” approach—Debt, Income, Mortgage, and Education—or more comprehensive needs analyses. These tools factor in inflation, investment returns, and expected duration of support.

Adjusting coverage over time is critical as life circumstances evolve. For example, coverage needs typically decrease as children become financially independent or debts are paid off. Conversely, coverage might increase due to new liabilities or changes in income. Insurance renewal and conversion options facilitate such flexibility without requiring new underwriting.

Additional Policy Features and Riders

Life insurance riders are optional add-ons that enhance or customize standard policies. Common riders include accidental death benefit, which provides an additional payout if the insured dies due to an accident; critical illness rider, which offers lump-sum payments upon diagnosis of specified illnesses; and waiver of premium, which suspends premium payments if the policyholder becomes disabled.

These riders increase policy costs but provide targeted financial protection. For instance, an accidental death rider is beneficial for high-risk occupations, while a critical illness rider integrates health coverage with life insurance.

Policyholders should weigh rider benefits against premium increases and consider their unique risk profiles. Insurance providers like RBC Insurance often bundle riders to create tailored solutions aligned with clients’ holistic financial plans.

When to Buy Life Insurance

Optimal timing for purchasing life insurance aligns with significant life events that increase financial responsibilities. Common triggers include marriage, childbirth, home purchase, or starting a business. Early purchase is advantageous due to lower premiums tied to younger age and better health.

Acquiring life insurance during one’s twenties or early thirties not only locks in favorable rates but also ensures coverage during years of accumulating debts and dependents. Conversely, waiting until later stages may result in higher premiums or insurability challenges due to health changes.

Regular reassessment of insurance needs is prudent, as life changes such as divorce, remarriage, or retirement may necessitate policy adjustments. Some permanent policies offer cash value that can be leveraged in retirement, demonstrating insurance’s versatility beyond death benefits.

FAQ

What happens if I outlive my term life insurance?

If the term expires while you are still alive, the coverage ends, and no death benefit is paid. You can often renew the policy at a higher premium or convert it to a permanent policy if your contract allows. Alternatively, you may choose to purchase a new policy, though health assessments may be required.

Can I convert term insurance to permanent insurance?

Yes, many term life policies include a conversion option that allows policyholders to switch to a permanent policy without additional medical underwriting. This feature is valuable for those whose insurance needs evolve but who want to maintain coverage without new health evaluations.

Is life insurance payout taxable?

Generally, death benefits paid to beneficiaries are not subject to income tax. However, if the policy has a cash value component or is used in certain investment arrangements, tax implications may arise. It is advisable to consult tax professionals to understand specific scenarios.

Who can be named as a beneficiary?

Beneficiaries can be individuals, trusts, charities, or entities chosen by the policyholder. Multiple beneficiaries with designated percentage shares are common. The policyholder can update beneficiary designations as circumstances change, ensuring alignment with estate planning goals.

Are medical exams always required for life insurance?

Not necessarily. While traditional underwriting often requires medical exams, some insurers offer no-exam policies with simplified underwriting. These tend to have higher premiums and lower coverage limits but provide faster approval, suitable for applicants seeking convenience.

Life insurance remains a cornerstone of financial security, offering customizable protection tailored to individual circumstances. As insurance products evolve, integrating features like cash value access and riders, policyholders benefit from enhanced flexibility. Prospective buyers should continuously evaluate their coverage in response to life changes and financial goals, leveraging tools and expert advice from reputable providers such as The Insurance Information Institute and Canadian insurers like Sun Life for informed decision-making.

Type of Insurance |

Coverage Duration |

Premium Structure |

Cash Value |

Typical Use Case |

|---|---|---|---|---|

Term Life Insurance |

1–30 years (fixed) |

Level or increasing over term |

No |

Income replacement during working years |

Whole Life Insurance |

Lifelong |

Fixed, level premiums |

Guaranteed growth |

Long-term protection and cash accumulation |

Universal Life Insurance |

Lifelong |

Flexible premiums |

Cash value based on interest/investments |

Flexible coverage with investment component |

Advertisement