Advertisement

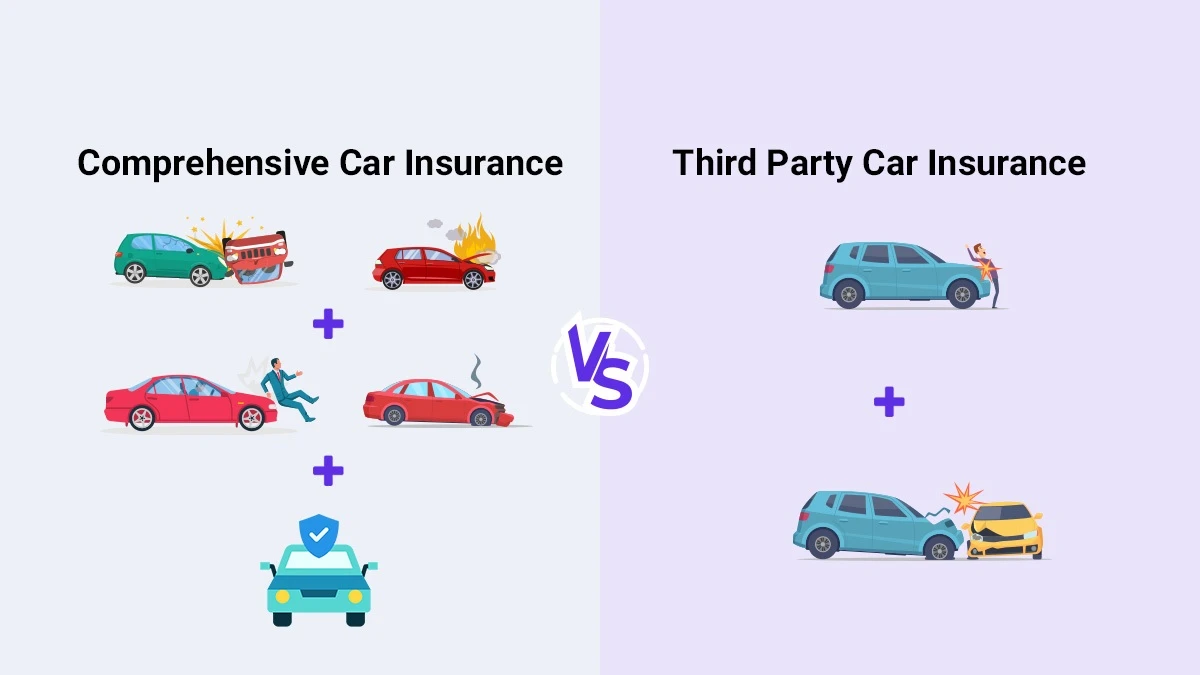

CRM Software – Third-party car insurance covers damages and injuries you cause to others but does not cover your own vehicle. Comprehensive insurance protects your vehicle from third-party liabilities plus damages from theft, natural disasters, vandalism, and other non-collision events, offering broader but more expensive coverage. Understanding the nuances between these two insurance types is critical for vehicle owners aiming to balance legal compliance, protection scope, and financial considerations.

third-party insurance primarily addresses liability claims arising from bodily injury or property damage inflicted on others by the policyholder. It does not cover any damage to the insured vehicle itself. In contrast, comprehensive insurance packages include this liability coverage and extend protection to the policyholder’s vehicle against a range of non-collision risks such as theft, fire, flood, hailstorms, or animal collisions. collision coverage, often confused with comprehensive insurance, is a separate policy component that indemnifies damage caused by crashes involving other vehicles or objects. Recognizing these distinctions informs better insurance decisions, especially considering regional legal mandates and personal risk profiles.

Understanding Third-Party vs Comprehensive Car Insurance

Third-party car insurance is the most basic form of vehicle coverage mandated in many jurisdictions worldwide. It insures the policyholder against legal liability for injuries or property damage caused to third parties in an accident where they are at fault. This insurance exclusively protects other road users and property owners, not the insured’s vehicle or personal injuries. Coverage typically includes medical expenses, repair costs for damaged vehicles or property, and legal defense costs in case of lawsuits. The policyholder’s vehicle damage or theft remains uncovered, exposing them to out-of-pocket expenses for repairs or replacement.

Advertisement

Comprehensive insurance encompasses third-party liability and incorporates extensive protection for the insured vehicle beyond collision events. It covers losses due to theft, vandalism, fire, natural disasters like floods and earthquakes, and damage from animals such as deer strikes. This type of policy is designed to mitigate a broader spectrum of risks that can affect a vehicle, making it especially valuable for newer or high-value vehicles. Comprehensive plans often include deductibles, which are fixed amounts the policyholder must pay before insurance coverage applies, influencing premium rates and claims processing.

Collision coverage, frequently bundled with comprehensive insurance, specifically addresses damage resulting from vehicle collisions with other cars or objects, regardless of fault. While comprehensive insurance protects against non-collision risks, collision coverage focuses solely on incidents where the vehicle impacts or is impacted by another object or vehicle. Understanding these distinctions is crucial since comprehensive and collision coverages differ in scope, claims criteria, and costs.

Legal Requirements and Regulatory Context

Third-party liability insurance is legally mandatory in numerous countries and provinces to ensure that drivers can compensate victims for injuries or property damage they cause. For example, in Canada, every province requires drivers to hold a minimum level of third-party liability insurance, with minimum coverage limits varying between provinces—Ontario mandates at least $200,000, while British Columbia requires $200,000 to $1 million depending on the situation. Similarly, in India, the Motor Vehicles Act mandates third-party liability insurance for all registered vehicles, with strict penalties for non-compliance. These regulations aim to protect victims and uphold public safety by ensuring at-fault drivers can cover damages.

Comprehensive insurance remains optional in most jurisdictions, valued as an add-on for enhanced protection rather than a legal obligation. Some regions, however, indirectly encourage comprehensive purchase by requiring proof of sufficient financial responsibility or through financing agreements mandating full coverage on leased or financed vehicles. The optional nature of comprehensive insurance allows vehicle owners to select coverage levels aligned with their risk tolerance, vehicle value, and financial situation.

Insurance laws and coverage requirements vary significantly by jurisdiction, affecting policy structures, premium calculations, and claims procedures. For instance, European countries often integrate third-party liability with mandatory personal injury protection, while U.S. states differ in minimum required coverage and optional add-ons. Understanding local legal frameworks is essential for compliance and selecting appropriate insurance products.

Coverage Comparison: What Each Policy Protects Against

Third-party insurance exclusively covers damages and injuries you cause to others. This includes bodily injuries to passengers, pedestrians, or other drivers and property damage such as damage to other vehicles, buildings, or roadside structures. It does not cover the policyholder’s own medical costs or vehicle repairs. For example, if you accidentally hit another car, third-party insurance pays for repairs to that car and medical expenses for its occupants, but you bear the repair costs for your own vehicle.

Comprehensive insurance covers a wider range of risks affecting your vehicle beyond collisions. Typical covered events include vehicle theft, vandalism, fire damage, and natural disasters such as floods, storms, hail, or earthquakes. It also protects against damage from hitting animals like deer or stray dogs. For example, if a tree branch falls on your car during a storm or your vehicle is stolen from a parking lot, comprehensive insurance covers the repair or replacement costs, minus any deductible.

Collision coverage, while often combined with comprehensive policies, specifically covers damage from collisions with other vehicles or stationary objects such as guardrails or poles. For instance, if you collide with another car or run into a ditch, collision coverage pays for repairs to your vehicle regardless of fault. This contrasts with comprehensive coverage’s focus on non-collision incidents.

Illustrating these differences, consider a scenario where a driver’s parked car is vandalized with graffiti. Third-party insurance offers no protection in this situation, while comprehensive insurance covers the repair costs. Conversely, if the driver hits another vehicle at an intersection, third-party insurance covers the damage to the other vehicle, but collision coverage (or comprehensive combined with collision) covers the driver’s own car repairs.

Financial Considerations and Cost Analysis

Premiums for third-party insurance are generally significantly lower than those for comprehensive coverage due to the limited scope of protection. Third-party insurance premiums can be 40-60% less expensive on average, making it attractive for owners of older vehicles or those with budget constraints. Deductibles in third-party policies are nonexistent or minimal, reflecting the policyholder’s limited coverage responsibilities.

Comprehensive insurance premiums reflect the broader risk profile and higher payout potential. Deductibles typically range from $250 to $1,000 or more, with higher deductibles lowering premium costs but increasing out-of-pocket expenses during claims. Insurers calculate premiums based on vehicle age, model, market value, driver history, location, and risk factors such as theft rates and weather exposure.

Vehicle age and market value critically influence the cost-benefit analysis of insurance choice. Older vehicles with depreciated values may not justify the higher premiums of comprehensive insurance due to the lower replacement costs and reduced risk of total loss. Conversely, high-value or newer vehicles benefit from comprehensive coverage that protects their investment and mitigates expensive repairs or replacement costs.

Additional coverage options or add-ons can enhance comprehensive policies, including roadside assistance, zero depreciation coverage (reimbursing full costs without depreciation deductions), and rental car reimbursement during repairs. These enhancements increase premiums but provide valuable convenience and financial protection in specific scenarios.

Practical Guidance for Choosing the Right Coverage

Selecting the appropriate insurance depends on evaluating your vehicle’s value, usage patterns, and personal risk tolerance. For older cars worth less than the annual comprehensive premium, third-party insurance often suffices, especially if the vehicle is primarily used for short trips or in low-risk areas. In contrast, owners of new or expensive vehicles, or those regularly driving in urban or high-theft areas, often benefit from comprehensive insurance.

Risk tolerance plays a significant role. Conservative drivers with safe driving records and limited exposure to natural disasters may opt for third-party insurance to minimize costs. Drivers in regions with frequent storms, floods, or high crime rates may require comprehensive coverage to protect against unpredictable losses.

Budget constraints can also dictate insurance choice. Comprehensive insurance typically requires higher premiums and deductibles, which might strain limited budgets. However, the cost of repairs or replacement without coverage can exceed these savings in the event of theft or natural disaster damage. Ensuring legal compliance with minimum third-party liability requirements remains non-negotiable.

Driver profiles influence recommendations: young or inexperienced drivers might prioritize comprehensive coverage due to higher accident risks, while older, budget-conscious drivers with low-risk profiles may prefer third-party insurance. Professional drivers or those who finance their vehicles often face lender requirements to maintain comprehensive coverage.

FAQ

What does third-party insurance cover exactly?

Third-party insurance covers liability for bodily injury and property damage you cause to others in an accident. It pays for medical expenses and repair costs for other parties but does not cover your own vehicle or injuries.

Is comprehensive insurance worth the extra cost?

Comprehensive insurance is worth the additional cost if you own a newer or high-value vehicle, live in areas prone to theft or natural disasters, or desire broader protection beyond liability. It mitigates financial risk from non-collision incidents that third-party insurance excludes.

Can I drop comprehensive insurance if my car is old?

Yes, many vehicle owners drop comprehensive coverage on older cars when the premium exceeds the vehicle’s value. This reduces insurance costs but exposes the owner to repair or replacement expenses from theft or damage.

How do deductibles affect my comprehensive coverage?

Deductibles are the out-of-pocket amounts you pay before insurance covers a claim. Higher deductibles lower premiums but increase your financial responsibility during claims. Choosing an appropriate deductible balances cost and protection.

What is the difference between collision and comprehensive insurance?

Collision insurance covers damage resulting from collisions with other vehicles or objects. Comprehensive insurance covers non-collision damage like theft, vandalism, fire, natural disasters, and animal impacts. Both can be combined for full protection.

—

Considering the evolving risk environment and advances in insurance technology, vehicle owners should periodically reassess their coverage needs. Integration of AI-driven risk assessment and telematics-based premium adjustments may soon influence tailored insurance offerings. For now, aligning coverage choice with vehicle value, legal requirements, and personal risk profile ensures optimal protection and financial prudence.

For more detailed comparisons and up-to-date legal requirements, consult authoritative sources such as PolicyBazaar’s comprehensive vs third-party insurance guide and GEICO’s overview on comprehensive coverage.

Advertisement