Advertisement

CRM Software – Car insurance premiums in Ontario represent the amount drivers pay annually to maintain their auto insurance coverage, averaging approximately $2,164 as of October 2025. This premium calculation incorporates multiple risk factors, including the driver’s record, vehicle characteristics, geographic location, coverage selections, and deductibles. Understanding these complex factors is essential for managing costs effectively in a province where insurance rates are among the highest in Canada due to claims frequency, regulatory frameworks, and market trends.

Premiums fundamentally serve as risk pooling mechanisms where insurance companies distribute potential costs of accidents and claims across a broad customer base. In Ontario, regulators like the Financial Services Regulatory Authority of Ontario (FSRA) oversee the approval of these rates to ensure they reflect actuarial fairness and market conditions. Premiums fluctuate annually, influenced by changes in inflation, claim costs, and shifts in driving behaviors, making the insurance landscape dynamic and requiring ongoing consumer awareness.

Understanding Car Insurance Premiums

A car insurance premium is the monetary charge paid by policyholders to insurers in exchange for protection against vehicle-related risks such as accidents, theft, or liability claims. This cost reflects the insurer’s assessment of risk exposure, balancing expected claim payouts with operational expenses and profit margins. Premiums correlate directly with coverage scope; more comprehensive policies with lower deductibles incur higher premiums, reflecting the increased insurer liability.

Advertisement

Risk pooling underpins premiums, where many drivers collectively share the financial risk of accidents. Insurers use actuarial models that analyze historical data, claims frequency, and risk factors to set premiums that are equitable yet competitive. Premiums must cover not only expected claims but also administrative costs and regulatory levies. Ontario’s car insurance system involves mandatory coverage elements, including third-party liability, accident benefits, and uninsured automobile coverage, each influencing the total premium.

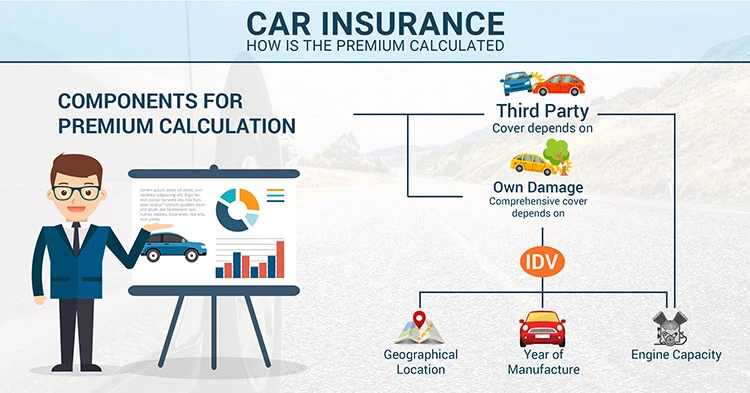

Key Factors Influencing Car Insurance Premiums

Driving record remains the most significant determinant of premium costs. Insurers evaluate past claims, traffic violations, and accident history to estimate future risk. A clean driving record can reduce premiums substantially, while recent claims or tickets often trigger premium surcharges. For example, a single at-fault accident can increase rates by 20% or more, depending on severity and insurer policies.

Vehicle characteristics such as make, model, year, and safety features critically affect premiums. Newer vehicles equipped with advanced safety technologies like automatic emergency braking, lane departure warnings, and anti-theft systems typically qualify for discounts due to lower claim probabilities. Conversely, high-performance or luxury vehicles attract higher premiums reflecting their repair costs and theft risk. Insurers also consider vehicle age; older cars may have lower premiums but higher deductibles.

Geographic location within Ontario influences premiums due to regional variations in accident rates, theft occurrences, and repair costs. Urban centers like Toronto generally experience higher premiums compared to rural areas, attributed to denser traffic and greater claim frequency. Some neighborhoods may have elevated risk profiles, leading insurers to adjust rates accordingly.

Coverage choices, including liability limits, collision, and comprehensive insurance, directly shape premium amounts. Opting for higher coverage limits increases premium costs, as does selecting lower deductibles that reduce out-of-pocket expenses during claims but raise insurer exposure. Deductible levels act as a balancing tool; increasing deductibles by $500 can reduce premiums by 10-15%, depending on the insurer’s rating model.

Usage patterns, such as annual mileage and vehicle use type (personal vs. commercial), are integral to risk assessment. Higher mileage correlates with increased accident risk, thereby elevating premiums. Usage-based insurance (UBI) programs like the my Drive™ program offered by insurers track driving behavior through telematics, rewarding safe drivers with discounts up to 20-25%. These programs analyze speed, braking, and time of day to provide personalized premiums.

Driver demographics, including age, gender, and credit score (where permitted), also impact premiums. Younger, inexperienced drivers typically pay higher rates due to elevated accident risk, whereas mature drivers with stable driving histories enjoy lower premiums. While Ontario does not use credit scores for premium rating, some provinces and insurers incorporate credit-based insurance scores to predict risk, affecting premiums accordingly.

Regional Variations in Canadian Car Insurance Premiums

Provincial differences in car insurance premiums result from varying regulatory environments, claims experiences, and market competition. Ontario’s average premium of $2,164 contrasts sharply with provinces such as New Brunswick ($971) and Nova Scotia ($891), reflecting differences in claim frequency, bodily injury claim costs, and insurer expense loads.

Regulatory frameworks contribute significantly to these disparities. Provinces with public insurance models, like British Columbia and Manitoba, often exhibit different premium structures compared to Ontario’s private insurance market. In Ontario, FSRA’s regulatory oversight mandates insurer rate approvals, ensuring premiums correspond to actuarial evidence while protecting consumers from excessive hikes.

Claims frequency and severity also drive regional variations. Higher traffic density and urban congestion in Ontario lead to more frequent claims, escalating overall premiums. Additionally, regional vehicle theft rates, repair costs, and weather-related risks—such as winter road conditions—impact insurer risk calculations and therefore premium costs.

Strategies to Lower Your Car Insurance Premium

Increasing deductibles effectively lowers premiums by transferring more initial claim costs to the driver. For instance, raising a collision deductible from $500 to $1,000 can reduce premiums by 10-15%, but drivers must be prepared for higher out-of-pocket expenses in the event of a claim. This strategy suits financially secure drivers with low claim likelihood.

Bundling home and auto insurance policies with the same provider generates multi-policy discounts, often ranging from 5-15%. Major insurers in Ontario such as TD Insurance, Belairdirect, and RBC Insurance offer bundling incentives that simplify management and reduce overall insurance costs.

Selecting vehicles equipped with advanced safety features and strong crash-test ratings reduces premiums by mitigating accident severity and repair costs. Insurers reward such choices because safer vehicles lower the probability of injury claims and expensive repairs. For example, cars with built-in collision avoidance and anti-theft devices may receive discounts of up to 10%.

Enrollment in usage-based insurance programs, like Intact Insurance’s my Drive™, provides customized premiums based on actual driving habits. These telematics-driven programs offer substantial savings for safe drivers, with discounts reaching up to 25%. Additionally, they encourage safer driving by providing feedback on speed, braking, and trip timing.

Maintaining a clean driving record remains the most reliable method to prevent premium increases. Avoiding traffic violations and at-fault accidents stabilizes rates and may qualify drivers for safe driving discounts. Some insurers offer accident forgiveness programs that limit premium hikes after a first incident.

Limiting annual mileage reduces exposure to accident risk and consequently premium costs. Drivers who use their vehicles less frequently typically benefit from lower premiums, especially when combined with UBI programs that track actual usage.

Regulatory Environment and Premium Rate Approval

The Financial Services Regulatory Authority of Ontario (FSRA) plays a pivotal role in overseeing auto insurance rates to balance insurer solvency with consumer protection. FSRA requires insurers to submit actuarial evidence supporting proposed premium rates, ensuring they reflect underlying risk without arbitrary increases.

Rate review processes involve analyzing claims data, loss ratios, and market conditions. FSRA may approve, reject, or request modifications to rate filings to maintain fairness and affordability. This regulatory oversight aims to prevent price gouging while enabling insurers to cover legitimate costs.

Consumer protections include transparency requirements, enabling policyholders to understand premium determinants and appeal unfair rate increases. FSRA also monitors insurer practices to prevent discriminatory rating factors and promotes public education on insurance cost drivers.

Market Trends Impacting Car Insurance Premiums

Inflation has significantly influenced premium increases over the past decade, with national average premiums rising 36.4% due to higher repair and medical claim costs. The increased price of vehicle parts, labour shortages in collision repair, and rising healthcare expenses contribute to escalating claim settlements.

Insurance fraud remains a persistent challenge, inflating premiums by increasing claim payouts unrelated to genuine losses. Insurers and regulators combat fraud through data analytics and collaboration with law enforcement, but residual effects continue to pressure premium levels.

Technological advances in telematics, AI-driven risk assessment, and automated claims processing improve underwriting precision, potentially stabilizing premiums by rewarding low-risk drivers more accurately. However, initial adoption costs may temporarily affect premium pricing.

The COVID-19 pandemic altered driving patterns, with reduced traffic volumes during lockdowns leading to fewer claims and some temporary premium reductions. As driving normalizes, insurers are adjusting rates to reflect post-pandemic risk profiles, including shifts toward remote work and changing vehicle usage.

FAQ

What determines my car insurance premium?

Your premium is determined by factors such as your driving record, vehicle make and model, geographic location, coverage level, deductible amount, and usage patterns. Insurers analyze these variables to assess your risk and set rates accordingly.

How can I lower my insurance premium without sacrificing coverage?

You can reduce premiums by increasing your deductible, bundling multiple insurance policies, choosing vehicles with advanced safety features, enrolling in usage-based insurance programs, and maintaining a clean driving record while limiting annual mileage.

Why do premiums increase after an accident or traffic ticket?

Accidents and traffic violations indicate higher risk to insurers, leading to increased premiums to offset the greater likelihood of future claims. The severity and frequency of incidents impact the extent of premium increases.

Are usage-based insurance programs reliable for saving money?

Yes, usage-based insurance programs like my Drive™ use telematics to reward safe driving with discounts typically ranging from 15% to 25%. They provide personalized premiums based on actual driving behaviour, benefiting low-risk drivers.

How often do car insurance premiums change and why?

Premiums usually change annually during policy renewal to reflect updated risk assessments, inflation, claims experience, and regulatory adjustments. Market trends and individual circumstances also influence rate fluctuations.

A car insurance premium is a dynamic figure shaped by multiple interrelated factors that insurers evaluate to balance risk and cost. Ontario drivers can manage premiums through informed vehicle choices, driving habits, and policy selections, leveraging regulatory protections and technological advances. As the insurance market evolves with inflationary pressures and innovation, staying informed and proactive remains key to optimizing insurance costs.

For more detailed insights on Ontario auto insurance rates and premium calculations, visit the Financial Services Regulatory Authority of Ontario and TD Insurance’s guide to premium calculations.

Advertisement