Advertisement

CRM Software – health insurance terminology defines the framework of how coverage operates, detailing the financial responsibilities and procedural rules that policyholders must navigate. Terms like deductible, copay, and coinsurance represent key components of cost-sharing, directly influencing out-of-pocket expenses. Provider networks—categorized as in-network or out-of-network—determine the pricing structure and access to care, with contracts between insurers and providers driving negotiated rates. Claims processing involves intricate billing procedures where allowable charges and coordination of benefits ensure fair payment distribution, particularly when multiple insurances are involved. A comprehensive grasp of these terms empowers consumers to make informed decisions, optimize their benefits, and avoid unexpected medical bills.

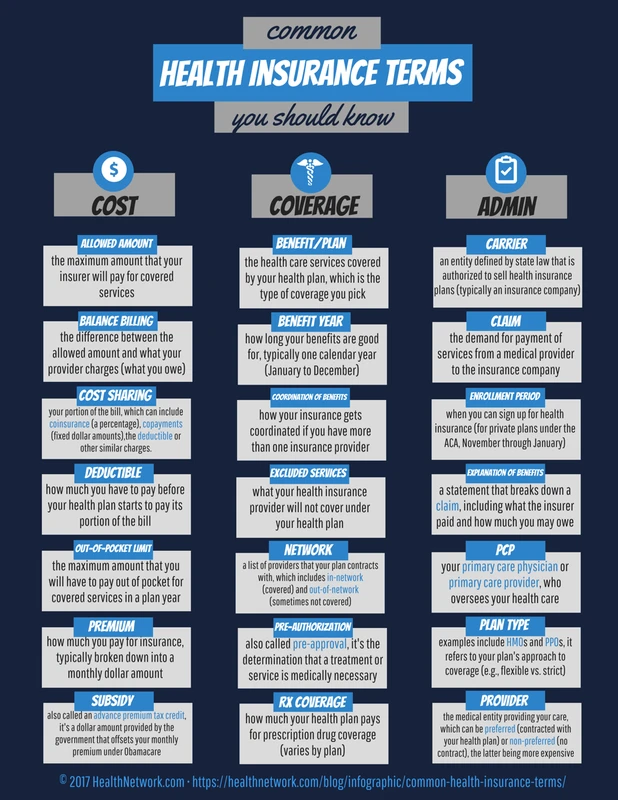

Deductibles specify the initial amount an insured individual must pay before insurance begins covering eligible expenses. For example, a $1,500 annual deductible means the insured pays the first $1,500 of covered services out-of-pocket. Copays are fixed fees charged per service, such as a $25 fee for a doctor’s visit, while coinsurance represents a percentage of costs shared after the deductible is met, commonly 20% paid by the insured and 80% by the insurer. The out-of-pocket limit caps total annual spending on covered benefits, protecting consumers from unlimited costs. These cost-sharing mechanisms reset annually, influencing how policyholders budget for healthcare.

Cost-Sharing Terms Explained

The deductible is a foundational cost-sharing element that directly impacts when insurance coverage kicks in. Policies often feature individual and family deductibles, with the family deductible being met collectively by all covered members. For instance, a family plan may have a $3,000 deductible that is satisfied through combined expenses from multiple members. Deductibles vary widely depending on plan design; high-deductible health plans (HDHPs) can exceed $4,000 annually, while traditional plans might have deductibles below $1,000. Importantly, preventive services under federal guidelines often bypass deductibles, offering free screenings regardless of deductible status.

Advertisement

Copays are straightforward fixed fees paid at the time of service, typically ranging from $10 to $50 depending on the service type. They incentivize appropriate utilization of healthcare by imposing manageable costs on routine visits or prescriptions. Coinsurance reflects shared financial responsibility after deductible fulfillment, with typical splits like 80/20 or 70/30. For example, after meeting a $1,000 deductible, if a $1,000 procedure has 20% coinsurance, the insured pays $200, and insurance covers $800. This percentage cost-sharing can significantly affect total medical bills, especially for high-cost procedures.

Out-of-pocket maximums provide a hard cap on yearly spending, including deductibles, copays, and coinsurance, but excluding premiums. Once reached, insurance pays 100% of covered costs. In 2024, federal regulations limit individual out-of-pocket maximums to $9,450 and $18,900 for family plans under Marketplace insurance, offering financial predictability amid costly health events.

Provider Networks and Their Impact

provider networks are central to controlling healthcare costs and access. In-network providers have negotiated contracts with insurers, offering discounted rates known as allowable charges. These rates are typically lower than billed charges, which represent the provider’s standard fees without insurer negotiation. For example, a specialist’s billed charge might be $500, but the insurer’s allowable charge could be $300. Patients using in-network providers benefit from lower copays and coinsurance.

Out-of-network providers lack contracts with the insurer, generally resulting in higher costs and increased patient responsibility. Insurers may reimburse only a portion of billed charges or apply usual, customary, and reasonable (UCR) rates, leaving patients liable for the balance, known as balance billing. The No Surprises Act, effective since 2022, limits unexpected out-of-network charges for emergency services and certain non-emergency care, protecting consumers from surprise medical bills.

Point-of-Service (POS) plans combine features of Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs). They require members to select a primary care provider (PCP) who manages referrals but allow some out-of-network coverage at higher cost-sharing levels. Managed care, encompassing HMOs, PPOs, and POS plans, emphasizes cost control and care coordination, often requiring prior authorization for specialized services to ensure medical necessity and cost-effectiveness.

Claims and Billing Processes

Claims represent formal requests by providers to insurers for payment of services rendered. A claim form details patient information, services provided, and charges. The insurer reviews claims against the policy terms, applying allowable charges and verifying coverage. When multiple insurances cover the same individual, coordination of benefits (COB) rules determine the order in which plans pay, preventing duplicate payments and minimizing out-of-pocket costs.

For example, if an individual has both employer-sponsored insurance and supplemental coverage, the primary insurer pays first up to its coverage limits. The secondary insurer may then cover remaining eligible costs. COB coordination requires accurate claim submission and sometimes additional documentation to resolve payment responsibilities.

Prior authorization is a utilization management tool requiring approval before specific services or medications to confirm necessity and coverage. Failure to obtain prior authorization can result in denied claims, increasing patient financial liability. This process varies by insurer and service type but is common for expensive procedures or specialty drugs.

Health Insurance Plan Types and Supplemental Coverage

Health insurance plans differ in structure, affecting access, costs, and flexibility. HMOs typically require members to use in-network providers and obtain PCP referrals, offering lower premiums and coordinated care. PPOs provide greater freedom to see out-of-network providers without referrals but at higher cost-sharing rates. POS plans blend these models, requiring PCP selection but allowing out-of-network care with increased costs.

Consumer-Directed Health Plans (CDHPs) pair high deductibles with Health Savings Accounts (HSAs), enabling tax-advantaged savings for medical expenses. HSAs empower consumers to manage healthcare spending directly, with funds rolling over annually and portability across jobs. This model encourages cost-conscious decisions but requires understanding complex plan features.

Supplemental health insurance covers gaps in primary insurance, such as dental, vision, critical illness, or accident insurance. These policies help manage out-of-pocket expenses not included in standard plans, improving financial protection against specific risks.

Regulatory and Legal Terms Affecting Insurance

The No Surprises Act, enacted in 2022, addresses unexpected bills from out-of-network providers during emergencies or non-emergency care at in-network facilities. It mandates insurers to cover these services at in-network cost-sharing rates and prohibits balance billing in such circumstances, significantly reducing consumer financial risk.

Federal programs like the Children’s Health Insurance Program (CHIP) provide coverage for low-income children, while COBRA allows temporary continuation of employer-sponsored insurance after job loss, albeit often at full premium cost. These programs supplement marketplace and employer plans by expanding coverage options.

Privacy regulations, notably the Health Insurance Portability and Accountability Act (HIPAA), govern the handling of personal health information within insurance transactions, ensuring confidentiality and data security. Grievance processes enable policyholders to dispute denied claims or coverage decisions, often involving internal reviews or external appeals.

Practical Tips for Consumers

Navigating insurance policies requires detailed review of plan documents, particularly the Summary of Benefits and Coverage (SBC), which outlines key terms like deductibles, copays, coinsurance, and provider networks. Consumers should verify provider networks before seeking care to minimize unexpected costs, using insurer directories or online tools.

Managing claims involves timely submission of documentation and understanding Explanation of Benefits (EOB) statements, which detail how claims were processed. Consumers should carefully review EOBs to detect errors or denials and promptly follow up with insurers or providers.

To avoid surprise bills, patients should inquire about provider network status and prior authorization requirements before procedures. Utilizing supplemental insurance and HSAs can also mitigate financial exposure.

FAQ

What is the difference between a copay and coinsurance?

A copay is a fixed fee paid at the time of service, such as $20 for a doctor’s visit. Coinsurance is a percentage of the cost shared between insurer and insured after the deductible is met, like paying 20% of a $1,000 bill.

How does coordination of benefits work?

Coordination of benefits determines which insurance pays first when multiple plans cover the same service, preventing duplicate payments. The primary insurer pays up to coverage limits, and the secondary insurer may cover remaining eligible costs.

What happens after I meet my deductible?

Once the deductible is met, you typically pay coinsurance or copays for covered services until reaching your out-of-pocket maximum. After hitting that cap, insurance covers 100% of eligible expenses.

Can I use out-of-network providers with my plan?

It depends on your plan type. PPOs and POS plans often allow out-of-network care at higher cost-sharing, while HMOs generally require in-network providers except in emergencies. Out-of-network services usually cost more.

What is a benefit year?

A benefit year is the 12-month period during which your insurance plan’s deductibles, copays, coinsurance, and out-of-pocket limits apply. After it ends, these amounts reset for the new period.

Understanding these terms and processes is vital for maximizing health insurance benefits and minimizing unexpected costs. As health insurance evolves with new regulations and market dynamics, staying informed and proactive remains the best strategy for consumers.

For further detailed explanations and official definitions, consult resources such as the CMS Health Insurance Terms Glossary and the Blue Cross Blue Shield Illinois Insurance Glossary.

Advertisement