Advertisement

CRM Software – Car insurance premiums are influenced by an intricate interplay of personal factors, vehicle characteristics, and environmental conditions. Central to determining your premium is your driving record, which insurers scrutinize to assess risk; a clean history can reduce rates significantly, while violations or past claims typically raise costs. Insurance providers also evaluate claims history, as frequent claims signal higher risk and often lead to premium increases. Beyond driver behavior, insurers analyze vehicle-specific data such as make, model, age, and safety ratings, all of which affect the likelihood and cost of repairs. Geographic location further modifies premiums due to variations in accident rates, theft incidents, and weather-related risks; urban areas generally incur higher costs than rural zones. This multi-dimensional risk assessment framework underpins how insurance premiums are calculated and highlights the actionable levers consumers can manipulate to lower their costs.

Telematics programs and pay-as-you-drive insurance models have revolutionized mileage-based savings by leveraging technology to tailor premiums according to actual driving behavior and mileage. These usage-based insurance (UBI) schemes employ devices or smartphone apps that monitor factors such as distance driven, speed, braking patterns, and time of day. By reducing annual mileage—especially below 10,000 miles—drivers may realize premium reductions averaging around $116 annually. Beyond mileage, maintaining safe driving habits in telematics programs can yield median savings of approximately $120, as insurers reward lower-risk behaviors. Eligibility for such programs often requires installing a telematics device or consenting to app-based tracking, with some providers offering trial periods or discounts to encourage adoption. Notable Canadian insurers like Desjardins and RBC Insurance have integrated telematics into their product offerings, enabling personalized premiums that reflect individual risk profiles rather than relying solely on generalized demographic data.

Adjusting coverage to align with your vehicle’s value and your risk tolerance can substantially cut insurance costs. For vehicles older than 15 years, dropping collision coverage often proves economical since repair costs may exceed the vehicle’s worth, and premiums for collision protection can be a significant portion of total costs. However, this approach carries the risk of bearing full repair expenses after an accident. Increasing deductibles from standard amounts like $500 to $1,000 or higher is another effective cost-saving strategy, with documented annual savings ranging from $464 to over $500 depending on insurer and region. This method shifts more out-of-pocket risk to the policyholder but lowers monthly premiums. A balanced decision requires evaluating your financial capacity to cover potential higher deductibles against premium reductions. Insurers typically allow customization of coverage components, enabling consumers to optimize policies for their circumstances while considering trade-offs between upfront premium savings and possible future expenses.

Advertisement

Bundling insurance policies is a widely recommended tactic to access additional discounts and streamline coverage management. Combining home and auto insurance with the same provider frequently qualifies for multi-policy discounts, which can reduce premiums by 5% to 15%, depending on the insurer. Similarly, multi-vehicle policies often attract discounts, incentivizing households with multiple cars to consolidate coverage. Safe driver discounts reward policyholders who maintain clean driving records over extended periods, sometimes coupled with completion of accredited defensive driving courses, which can reduce premiums by 10% or more. Loyalty programs offered by some insurers provide incremental savings or benefits for maintaining continuous coverage, though consumers should remain vigilant for competitive quotes from alternative providers to avoid overpaying. Switching insurers can yield substantial rate reductions, especially when combined with bundling and discount strategies, but assessing coverage quality and service is critical to avoid underinsurance.

Vehicle-specific factors such as make, model, and safety ratings exert a measurable impact on insurance premiums. Cars with higher safety ratings, equipped with advanced driver-assistance systems (ADAS), and lower theft rates typically command lower premiums due to reduced accident and repair risks. Conversely, luxury models or performance vehicles often attract higher premiums because of increased repair costs and greater likelihood of theft or speeding violations. Geographic location remains a pivotal determinant; urban dwellers face higher premiums due to elevated collision frequency, vandalism, and theft risks, with some urban areas recording premiums 20% to 30% above national averages. Repair costs also vary regionally and by vehicle type; vehicles with expensive or hard-to-source parts incur higher premiums. Insurers integrate these variables into actuarial models to adjust rates accordingly, underscoring the importance of considering both vehicle choice and residence when seeking cost-effective coverage.

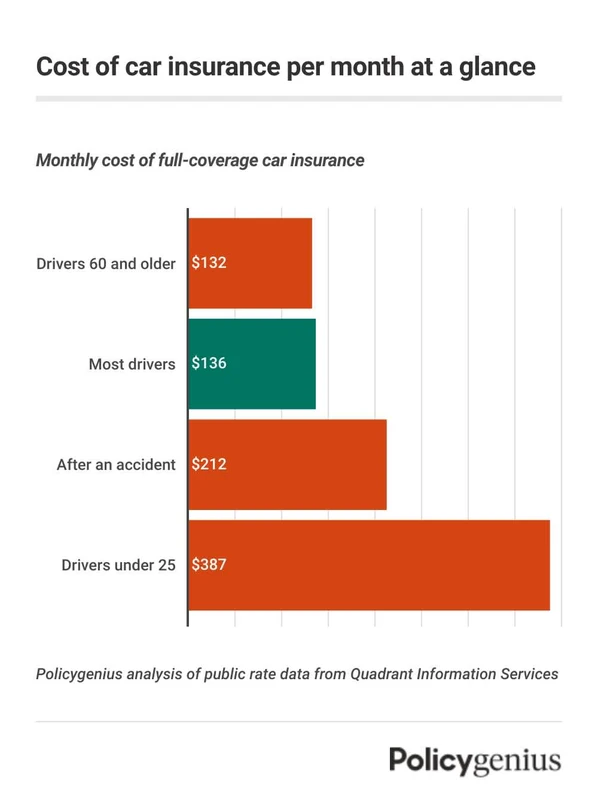

Life changes and evolving vehicle usage patterns necessitate timely policy updates to optimize premiums. Removing teen drivers from policies once they gain independent coverage can save families from $1,500 to $2,000 annually, as young drivers typically attract high premiums due to increased risk. Marital status changes—such as marriage or divorce—also influence rates, with married drivers often benefiting from lower premiums due to perceived stability. Remote work and retirement frequently reduce annual mileage, representing an opportunity to adjust policies to lower premiums by reporting decreased use or switching to mileage-based plans. Failure to update policies with these life changes can result in overpaying for coverage that no longer reflects actual risk. Insurers encourage policyholders to review and revise coverage periodically to ensure alignment with current circumstances and financial goals.

Maintaining a clean driving record remains the cornerstone of affordable car insurance, with accident-free and violation-free histories translating directly into lower premiums. Accredited defensive driving courses offer tangible benefits by demonstrating commitment to safe driving, which insurers often reward with discounts. Additionally, experienced drivers with longer driving histories generally secure better rates, as actuarial data shows reduced risk over time. Conversely, traffic violations, at-fault accidents, and claims inflate premiums significantly and may trigger policy non-renewals or surcharges. Some insurers incorporate driver coaching or telematics feedback to help policyholders improve habits, thereby reducing risk and premiums over time. This dynamic incentivizes ongoing commitment to safety as a sustainable method for lowering insurance expenses.

Consulting insurance brokers or representatives enhances the ability to navigate complex policy options and uncover personalized savings opportunities. Brokers provide expertise in comparing multiple providers, understanding policy nuances, and negotiating terms tailored to individual risk profiles. Additionally, technology-driven solutions—such as smartphone apps and onboard telematics devices—offer real-time monitoring and feedback to optimize driving behaviors and premiums. Regular policy reviews, ideally annually or following major life events, ensure continued alignment of coverage with evolving needs and market conditions. Insurers increasingly leverage artificial intelligence and data analytics to refine premium calculations, making informed consultations and technology adoption essential for maximizing cost efficiency.

Cost-Saving Strategy |

Estimated Annual Savings |

Key Considerations |

|---|---|---|

Increase Deductible from $500 to $1,000+ |

$464 – $500+ |

Higher out-of-pocket costs; suitable for financially prepared drivers |

Reduce Annual Mileage Below 10,000 Miles |

Approx. $116 |

May require lifestyle adjustments; eligibility for usage-based insurance |

Enroll in Telematics Programs |

Median $120 savings |

Requires consent to monitoring; rewards safe driving behaviors |

Drop Collision Coverage on Vehicles 15+ Years Old |

Varies; potentially hundreds annually |

Risk of full repair costs after accidents |

Remove Teen Drivers |

$1,500 – $2,000 |

Apply when teen gains independent coverage |

Bundle Home and Auto Insurance |

5% – 15% |

Requires multiple policies with same insurer |

The table above outlines primary car insurance savings strategies, illustrating potential financial impact alongside essential trade-offs to consider before implementation.

FAQ

How does increasing my deductible lower car insurance premiums?

Increasing your deductible means you agree to pay more out-of-pocket before insurance coverage kicks in, which lowers your insurer’s risk and typically reduces your premium. However, it also means higher costs if you file a claim, so consider your financial ability to cover the increased deductible.

What is usage-based insurance and how can it save me money?

usage-based insurance (UBI) uses telematics technology to monitor your driving habits and mileage. Safer drivers who drive less may receive personalized discounts based on actual risk, leading to savings compared to traditional insurance pricing models.

Is dropping collision coverage a good idea for older vehicles?

For vehicles over 15 years old with low market value, dropping collision coverage can reduce premiums significantly. The downside is that you will have to pay for repairs out of pocket in case of an accident, so evaluate your risk tolerance and financial situation.

How does bundling home and auto insurance affect my premiums?

Bundling policies with the same insurer often qualifies you for multi-policy discounts, reducing premiums by 5% to 15%. It also simplifies management but requires maintaining multiple policies with the same provider.

Can removing a teen driver from my policy really save that much?

Yes, teen drivers are typically high-risk and expensive to insure. Removing them once they have their own coverage can save families between $1,500 and $2,000 annually depending on the insurer and region.

Lowering car insurance costs effectively requires a multifaceted approach that leverages technology, adjusts coverage to your actual risk, and accounts for personal and vehicle-specific factors. As the insurance market evolves with data-driven personalization and telematics adoption, consumers who actively manage their policies, embrace usage-based programs, and maintain safe driving habits will continue to unlock substantial savings. Consulting insurance professionals and utilizing digital tools remains crucial in optimizing coverage and premiums in 2026 and beyond.

For further detailed strategies and up-to-date insights on car insurance savings, visit CBC’s car insurance tips and Consumer Reports on lowering car insurance rates.

Advertisement